The main point of this article is at the very end…but you gotta read all of this article to understand that question…and to know why it’s so important.

The main point of this article is at the very end…but you gotta read all of this article to understand that question…and to know why it’s so important.

I have held off writing this post for over a week…didn’t think I would write it at all. By the time is posts it will be more like 10 days. And I was sure I wouldn’t write it “in the open” vs a “Patriot” article…but last night (Friday – 5/1) changed my mind…$4.69 per gallon gas! And I am going to write it in the open that maybe some folks would read it that might not otherwise invest their time to do so.

Just a quick review…gas here locally hit $3.09 per gallon shortly after Trump became President…nice! It was about a 6% drop in price…SWEET! Then Trump decided to go on the war path…first bombing Iran, then overthrowing Valenzuela, then start the full-on war with Iran a couple of months ago. Now gas is $4.69 per gallon…over 50% increase in the price of gas!!!!

So what does that actually mean?

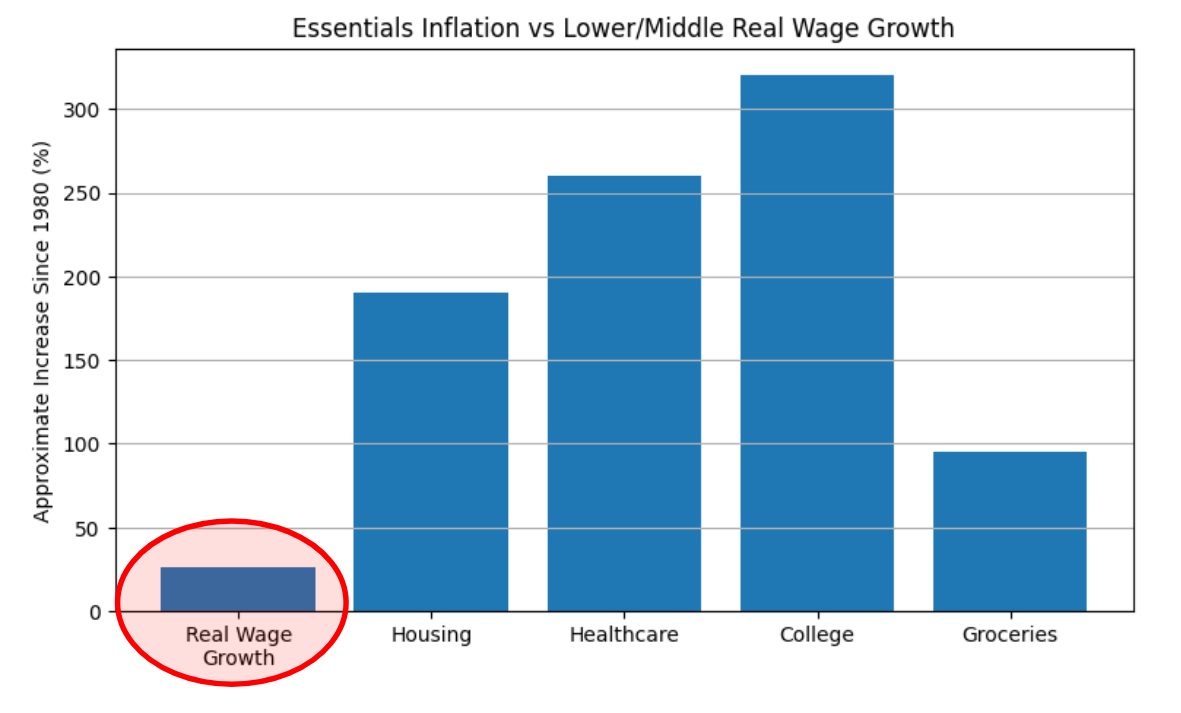

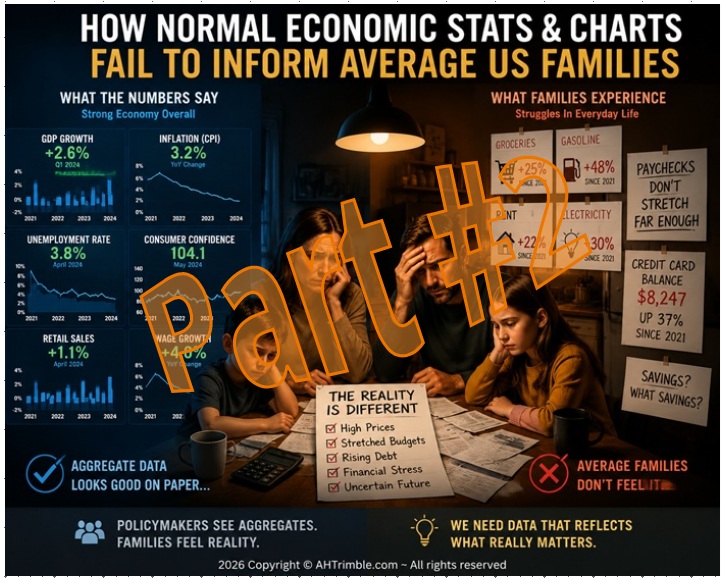

In 2024, under President “Sleepy Joe” Biden, the average US family of 4 used about 1,600 gallons of gas per year. Gas  back then was about $3.29 per gallon. That meant that family of 4 spent about $5,200 for gas, about $430 per month. Hurts for sure…but it could be worse. In 2025 the price of gas went up and consequently the US consumption of gas went down.

back then was about $3.29 per gallon. That meant that family of 4 spent about $5,200 for gas, about $430 per month. Hurts for sure…but it could be worse. In 2025 the price of gas went up and consequently the US consumption of gas went down.

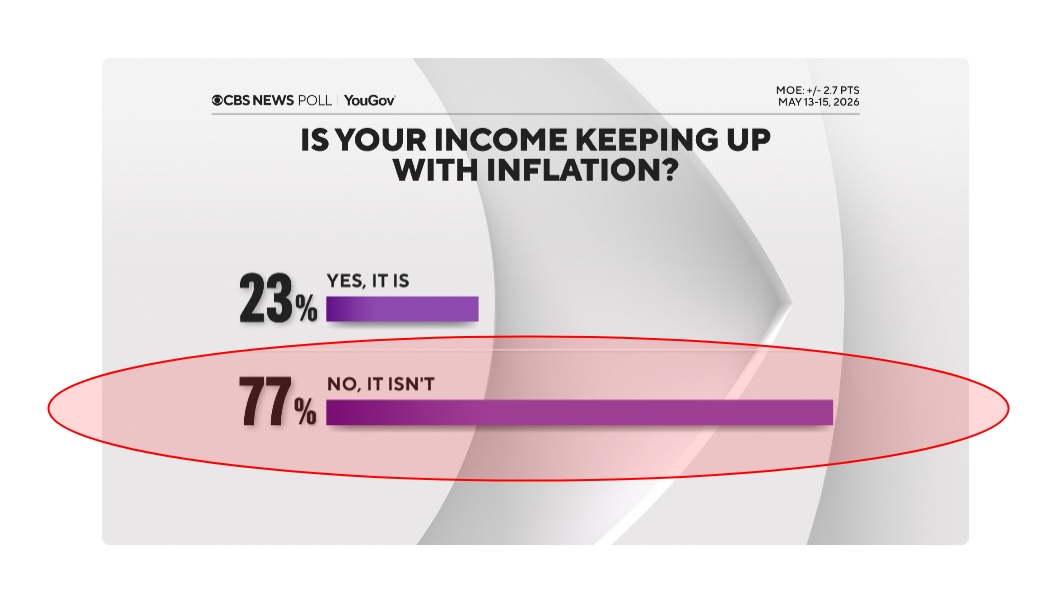

Now, in 2026 under President Trump, the same US family of 4 is using about 110 gallons of gas per month…about 1,300 gallons annualized…a reduction of 300 gallons per year. And now gas is $4.69 per gallon…that means that family is now spending $6,100 per year for gas. That is an increase of over 17% out of their budget for gas. Oh, wait…due to the huge price increase in gas that same family is now using 18% less gas. So that family goes fewer places and pays way more. Ugly!

Think about it…if that family drove the same amount in 2026 (Trump) as 2024 (Biden)…$2,300 more per year for gas under Trump!!!

For what it’s worth…

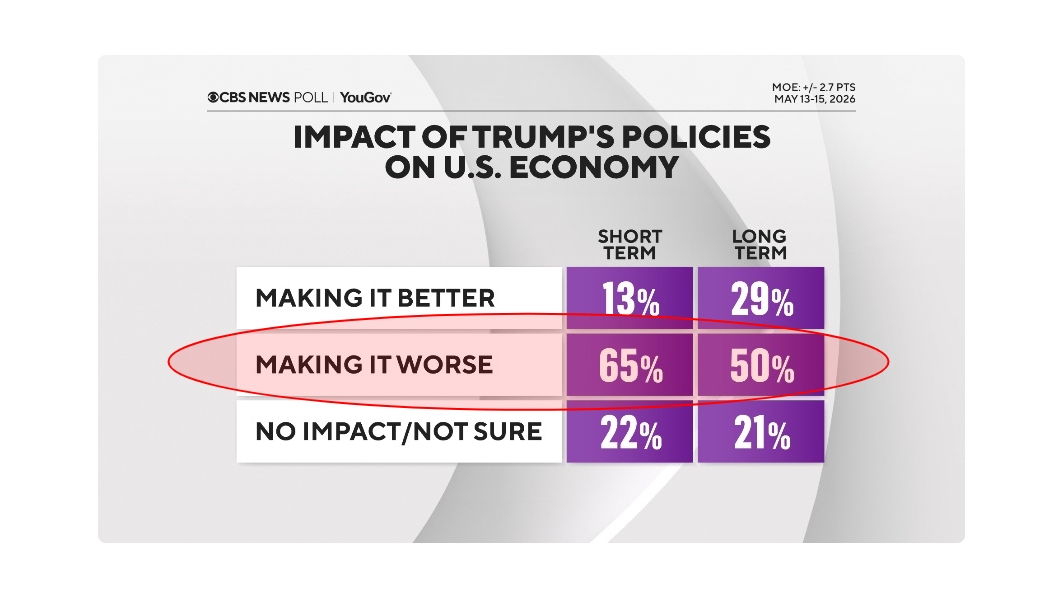

Inflation rate in 2024 was 2.9%……Inflation rate in 2026 is 3.3%

What does that have to do with anything other than me whining and complaining? Yeah…hang on…

Does Gannon Ken Van Dyke ring a bell? Yeah, he bet more than $33,000 on the prediction/betting website Polymarket just days before President Donald Trump announced Maduro’s capture (President of Valenzuela). Van Dyke is also a Special Forces operator working for the US military. His series of bets, $33000, netted him more than $400,000. Van Dyke was recently arrested and the DOJ charged him with unlawful use of confidential information for personal gain, theft of nonpublic government information, commodities fraud, and wire fraud.

Did you catch “Polymarket”…the place where he placed his bets? A little info from my March 30th post:

Polymarket –

- 2020 Polymarket began operations as a company…same year Trump announced his 2024 bid for President.

- 2022 Polymarket was denied the ability to do business in the U.S. by the Federal Trade Commission (FTC).

- Early August 2025 Trump family invested in Polymarket, estimates are an 8-figure amount ($10million+).

- Later in August 2025 Donald Trump, Jr is given a seat on the board of Polymarket with undisclosed salary.

- September 2025 Polymarket became authorized to relaunch business in the US…by the FTC via the Trump Administration (Donald Trump, Jr’s, father…President Trump).

- While it isn’t publicly disclosed how much Trump, Jr. is additionally paid as an “advisor”, insider estimates run as high as a million dollars per year…in addition to the Trump ownership position.

- Polymarket is a global cryptocurrency-based prediction/betting market, headquartered in Manhattan, New York City. It offers a platform where individuals can place bets on future outcomes, economic indicators, awards, political and legislative outcomes, and military conflicts. Participants can deposit cryptocurrency through the Polygon blockchain network

and bet the likelihood of specific future outcomes…including betting on military strikes and ongoing wars.

and bet the likelihood of specific future outcomes…including betting on military strikes and ongoing wars.

Did you catch that yet? Trump family invests millions to become a partner in Polymarket, son of President Trump gets a seat on their board, and Polymarket gets approved to do business in the US. Then Trump family proceeds to makes millions off of Polymarket business. But, Van Dyke makes $400k and gets charged with…unlawful use of confidential information for personal gain, theft of nonpublic government information, commodities fraud, and wire fraud…all felonies. Huuummmm………ahhhhhhh…….

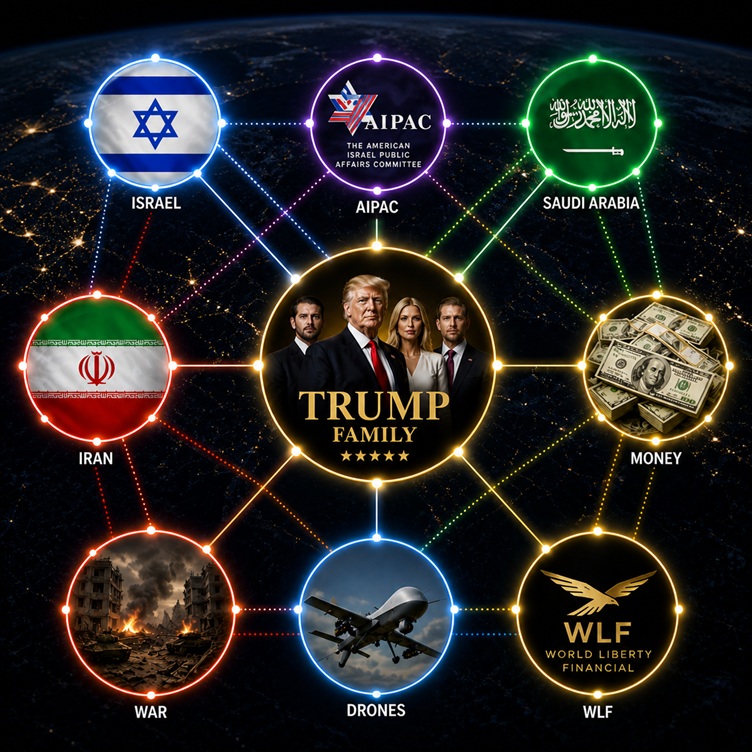

Oh, did you miss the “cryptocurrency” currency part of Polymarket’s business? World Liberty Financial (WLF) is part of the  cryptocurrency world…and owned by the Trump family. Oh wait…billionaire Justin Sun, who invested in WLF, filed a lawsuit 3 weeks ago in a California federal court, alleging that his multi-million dollar investment was procured through fraud and the project is now “on the verge of collapse.” So the Trump family makes billions with WLF…investors lose millions….Van Dyke goes to prison.

cryptocurrency world…and owned by the Trump family. Oh wait…billionaire Justin Sun, who invested in WLF, filed a lawsuit 3 weeks ago in a California federal court, alleging that his multi-million dollar investment was procured through fraud and the project is now “on the verge of collapse.” So the Trump family makes billions with WLF…investors lose millions….Van Dyke goes to prison.

But there is more…

Zach Witkoff is one of the main managers of WLF. Zach Witkoff is the son of Trump’s Middle East Envoy Steve Witkoff.Yeah, Steve is the guy working closely with Saudi Arabia for additional business deals on behalf of the Trump family business. And guess what…Saudi Arabia and Iran are long-time rivals and often considered enemies. They compete for power and influence in the Middle East and support opposing sides in regional conflicts (like Yemen and Syria). They also represent different branches of Islam: Saudi Arabia is Sunni and Iran is Shia…a long-time, long-running religious feud…okay, most of the time it is violent differences.

Hang on…more…

Steve Witkoff is Jewish and aligns with Israel in all policy maters. And the Trump family business has business interests in Saudi Arabia and trying to establish large real-estate business deals in Israel. And Steve Witkoff has been involved with the Iran War even before it was the Iran War making unrealistic demands of Iran…and he was on the US negotiation team that was negotiating with Iran to end the war…which hasn’t ended.

Would you like to connect those dots? Yeah…pretty easy to do!

Here we go…a bit more for you…

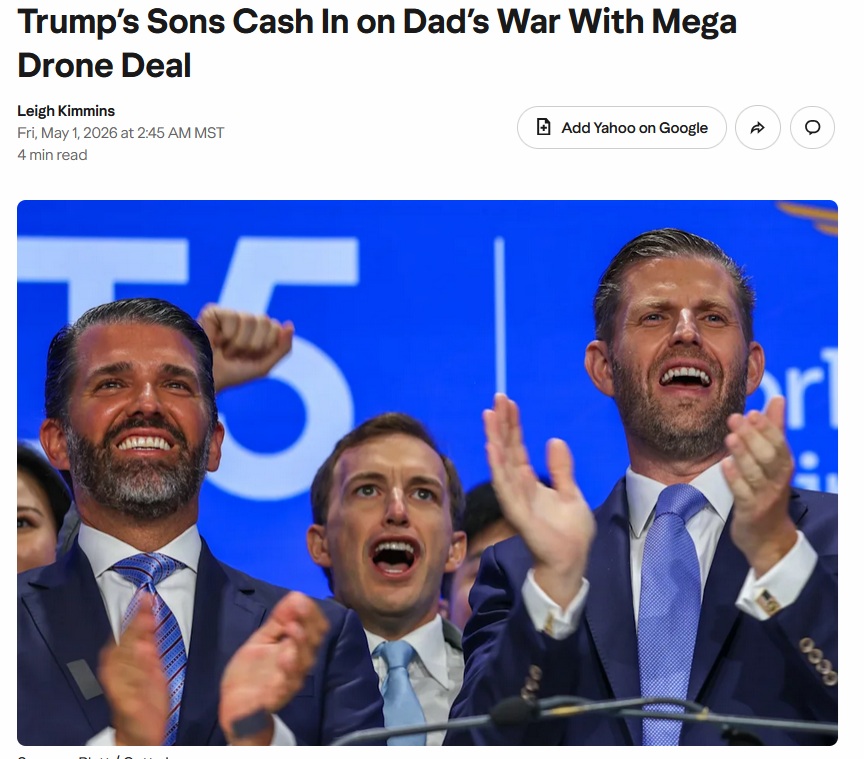

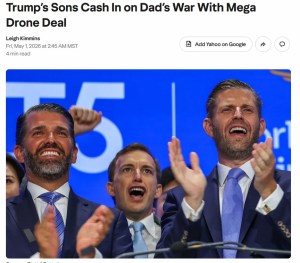

Back in March I explained how the Trump Family business bought into two different drone companies in 2025…one of which is located in Israel. And I said then that they would get US government contracts. Yeah,  last month Eric Trump, the public head of the Trump family business and President Trump’s son, announced that the Pentagon…wait for it…awarded the Trump family drone business a $24million contract…that’s just the start.

last month Eric Trump, the public head of the Trump family business and President Trump’s son, announced that the Pentagon…wait for it…awarded the Trump family drone business a $24million contract…that’s just the start.

What did the price of gas have to do with the rest of the article? Same thing as Gannon Ken Van Dyke does.

See, while Donald Trump is President the Trump family makes 10’s of millions in one deal, then hundreds of millions in another, and then billions in yet another Trump family business deal…and what happens to the schmuck Van Dyke who made a couple hundred thousand through one of Trump’s businesses? He’s going to prison. And then there is that average American family who gets hit for thousands of dollars more per year for gas…while the Trump family makes BILLIONS of dollars.

How do the Trumps make it?

Ah, starting a war with Iran who just happens to be hated by both Israel and Saudi Arabia…and there just happens to be a quiet overlap of interests between Israel and Saudi Arabia. Despite some tensions, there are still areas of indirect alignment between the two…and guess who is in the middle of it? Steve Witkoff (Jewish and huge supporter of Israel) happens to be involved as Trump’s “envoy” with Iran. And then Polymarket (Trump family business) makes millions off of predictions regarding the war. And then Trump family drone business (part of which is in Israel) gets a Pentagon contract for ten’s of millions…replacing drones used by Israel and the US in a war that Trump started. And the Saudi’s are a huge investor in Trump’s cryptocurrency company (run by Steve Witkoff’s son) and a partner with Trump in real-estate deals in Saudi Arabia. Oh, let’s not forget…the on-going negotiations between the Trump family business and Israel for real-estate deals located in Israel…while the US, at Trump’s direction, bombs the shit out of Iran…Israel’s and Saudi Arabia’s mortal enemy.

Who says Trump is bought and paid for???? Let’s talk Miriam Adelson (born Miriam Farbstein, 1945)…she is a Jewish dual citizen Israeli-American physician, multi-multi-billionaire, and political donor. And she just happened to donate $130million to Trump’s 2024 Presidential campaign. Adelson makes frequent visits to the White House and Trump himself credited Adelson with helping shape U.S. decisions on Israel policy. Oh, FWIW…AIPAC spent another $150million during the 2024 campaign…gotta get ’em to send more $’s and bombs to Israel! Can’t let that genocide slow down…oh, no.

Hey, did you know…Miriam Adelson received the Presidential Medal of Freedom on November 16, 2018, from Donald Trump. She got it for “especially meritorious contributions”, “serving U.S. national interests” and “world peace”. Imagine that. Did you also know that Adelson gave $25million in contributions to Trump’s first campaign…his single largest donor. Coincidence?

Okay…here’s the big question…the one I told you about at the beginning of this article…

Remember Conservatives and MAGA folks were screaming about the Biden Crime Family? You know…the Biden family benefiting 10’s of millions of dollars from Biden being Vice-President and then President. All the uproar how that they should be investigated and people should go to prison…specifically Hunter Biden, Joe’s son…remember all of that? I do…I wrote a lot about it…a crime family pure and simple.

Remember Conservatives and MAGA folks were screaming about the Biden Crime Family? You know…the Biden family benefiting 10’s of millions of dollars from Biden being Vice-President and then President. All the uproar how that they should be investigated and people should go to prison…specifically Hunter Biden, Joe’s son…remember all of that? I do…I wrote a lot about it…a crime family pure and simple.

Wait for it…

So what is the difference between the Biden Crime Family and the Trump Crime Family? Well, other than the Bidens only making 10’s of million and the Trumps making billions? Where is MAGA now? Why aren’t they screaming “criminals” now?

It’s all about a gap between what someone says and what they actually do. Hypocrisy is when someone says they believe in certain values or rules, but they behave in a different way when it goes against them.

It’s all about a gap between what someone says and what they actually do. Hypocrisy is when someone says they believe in certain values or rules, but they behave in a different way when it goes against them.

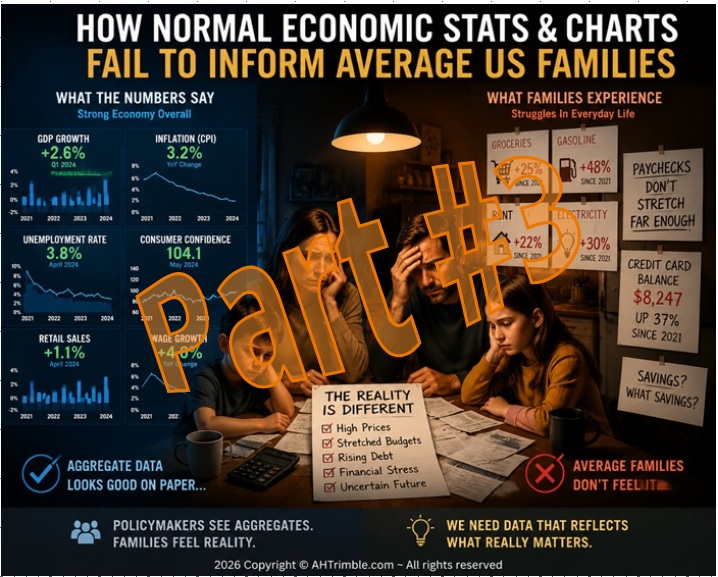

Think what might happen if people would connect all the dots?I wonder if it would look something like this if they were realistically artistic…

Nah…couldn’t possibly be true…right?

Nah…couldn’t possibly be true…right?

Then again, some people will never allow their brain to connect these dots, nor will they see reality for what it really is.

Here is something for those who are interested…

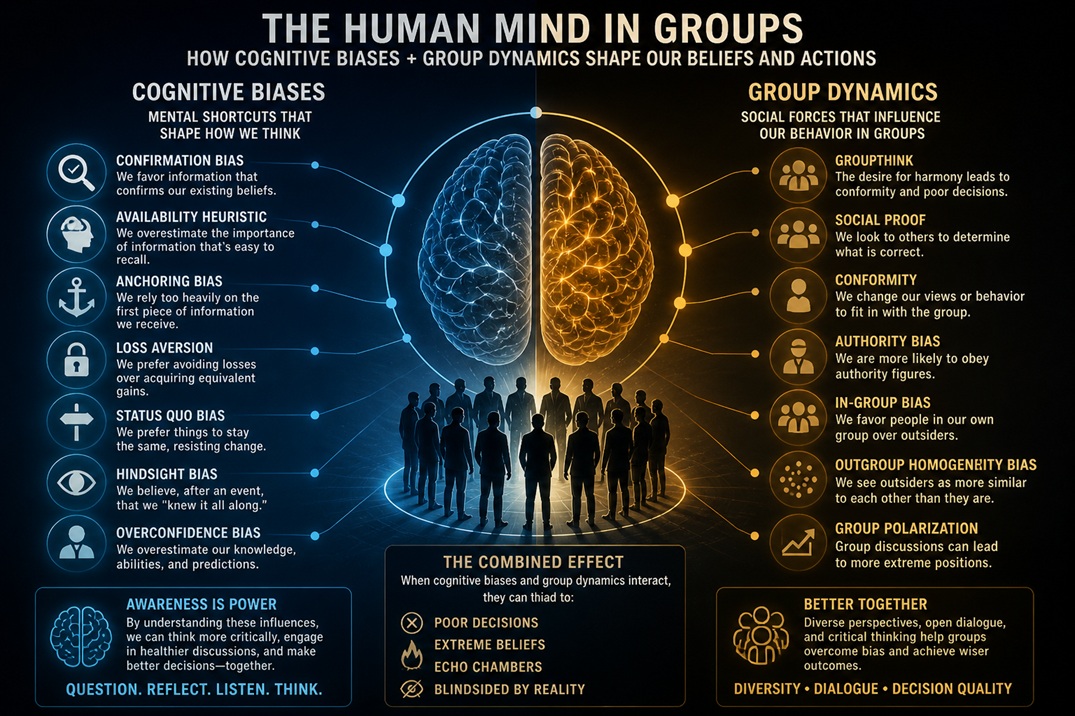

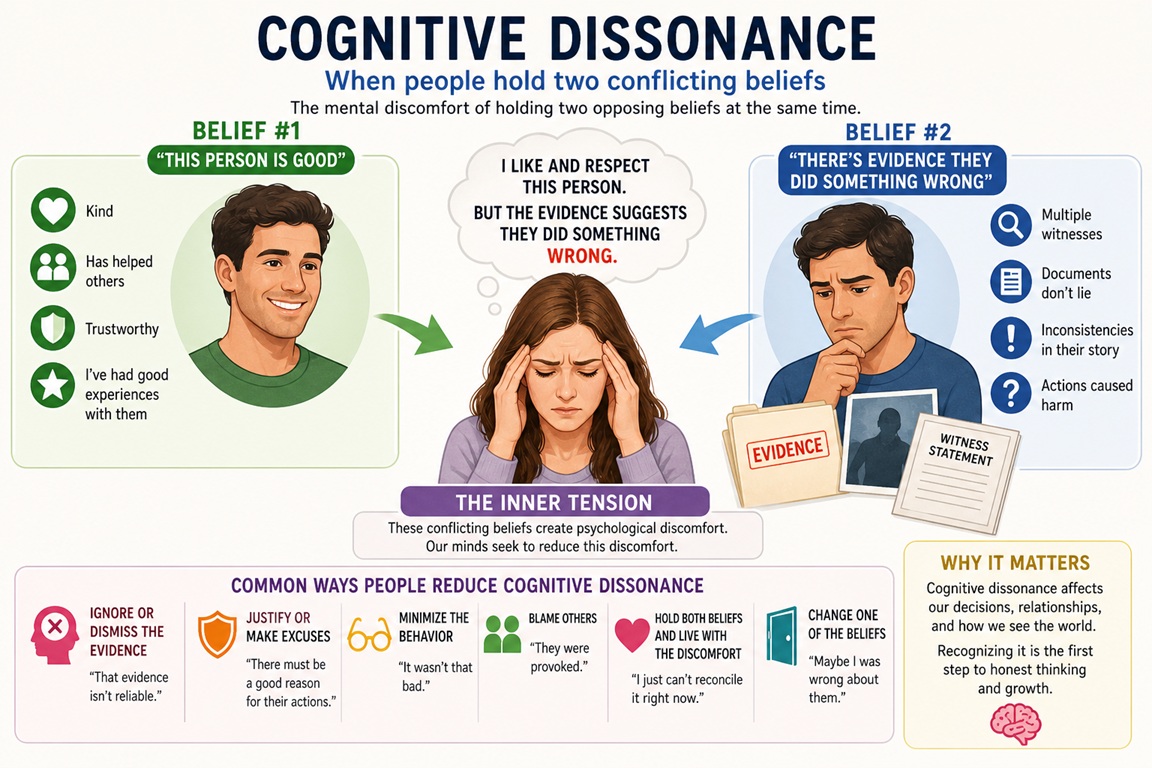

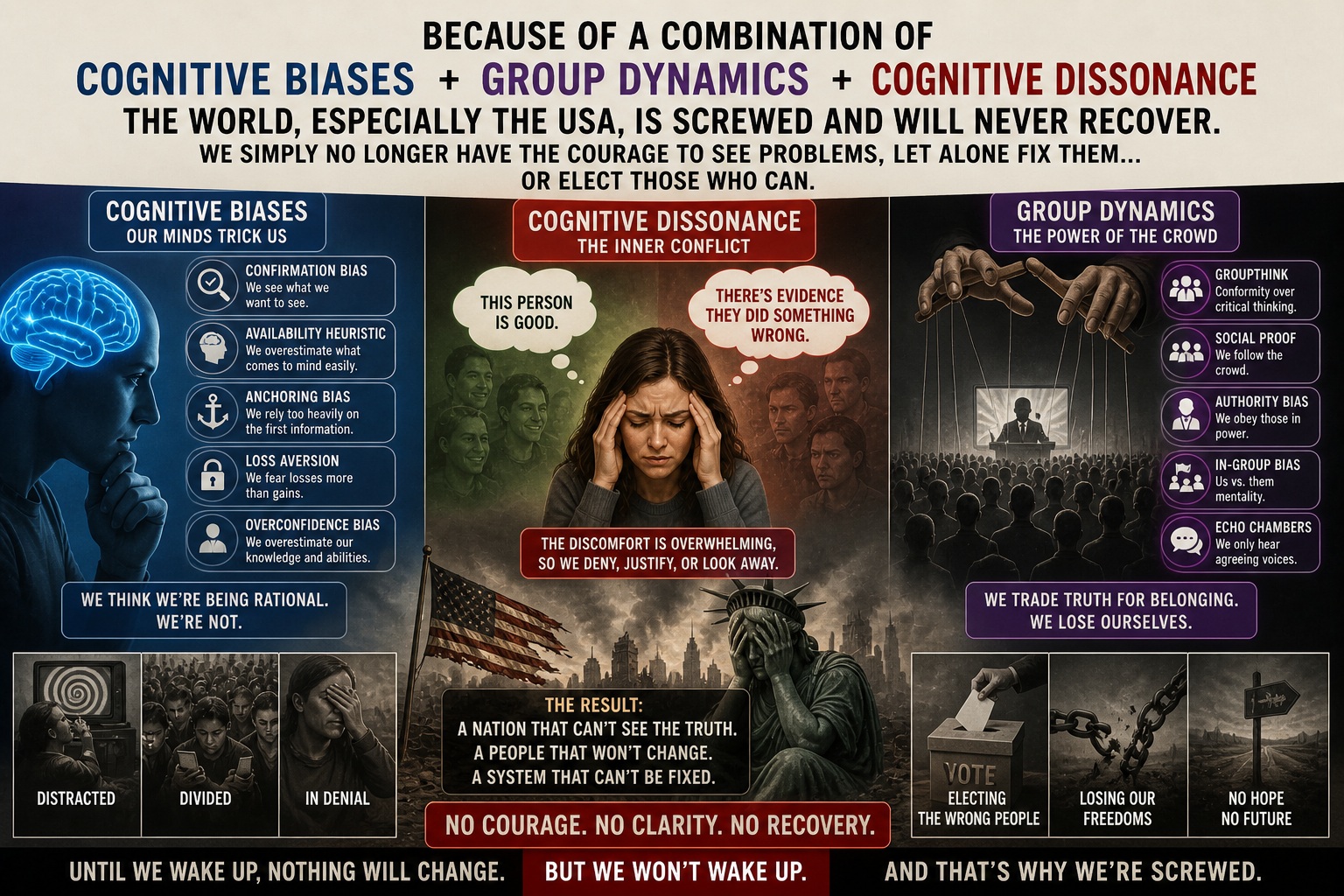

A combination of cognitive biases and group dynamics is not a single diagnosis of a mental illness. People can genuinely believe something -even against strong evidence- because of how the human mind processes identity, loyalty, and information. This phenomena is stronger in politics because politics isn’t just about facts, it’s tied to identity, emotion, and social belonging in a way most everyday issues aren’t. Political issues are complicated because most people don’t have time to deeply research everything. So they rely on those they trust…leaders, media sources, and group consensus (group think).

That makes it easier for beliefs to stick…even if flawed or outright wrong…it’s called “confirmation bias”. Cognitive dissonance also comes into play…when people hold two conflicting beliefs (i.e. “this person is good” vs. “there’s evidence they did something wrong”). To reduce/avoid discomfort, they may reject the evidence, reinterpret facts to match their views, and/or double down on their beliefs.

That makes it easier for beliefs to stick…even if flawed or outright wrong…it’s called “confirmation bias”. Cognitive dissonance also comes into play…when people hold two conflicting beliefs (i.e. “this person is good” vs. “there’s evidence they did something wrong”). To reduce/avoid discomfort, they may reject the evidence, reinterpret facts to match their views, and/or double down on their beliefs.

Bottom line…in everyday situations, changing your mind takes minimal effort and costs little. But, with politics, changing your mind can feel like losing your identity, your group abandoning you, and losing the “fight”. So people often hold on tighter to their political beliefs, even when facts, statistics, and evidence show them they are wrong.

Sad, isn’t it…

Sad, isn’t it…

There is one option that will work…

There is one option that will work…

Always the right answer, always the right solution, always the right choice.

Always the right answer, always the right solution, always the right choice.

Related Articles –

2009 - 2026 Copyright © AHTrimble.com ~ All rights reserved

No reproduction or other use of this content

without expressed written permission from AHTrimble.com

No legal, economic, or financial advice is given, no expertise to be assumed.

I may receive compensation from advertised/mentioned products on this website.

See Content Use Policy for more information.