You should probably read the previous two parts before reading further…it will make much more sense:

< click here to read Part #1 >

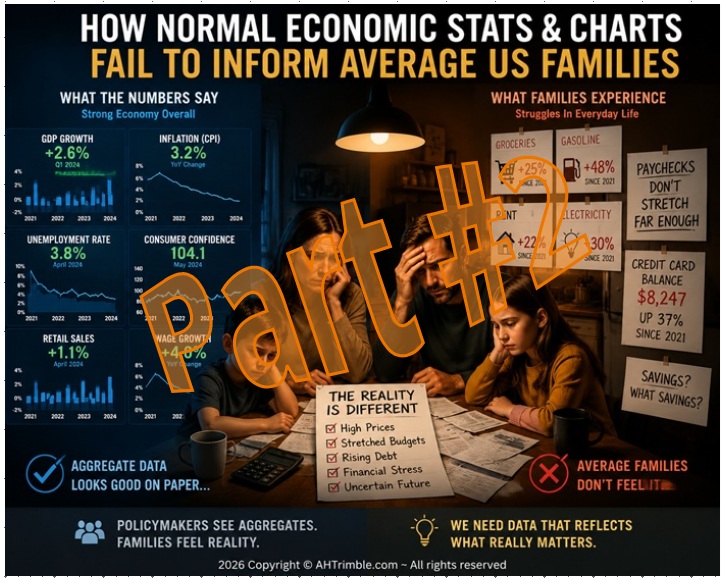

< click here to read Part #2 >

So now is the time when I get into the nitty-gritty of this economic stuff…wrap it up in a neat pristine package where everything makes sense and all the world becomes sunshine and butterflies. Well…maybe not.

But, what I will do is share some additional thoughts and then layout some ideas that every family, every person can do to reduce the negative impact of what is happening. Now, you will have to bear with me a bit, it doesn’t come quick.

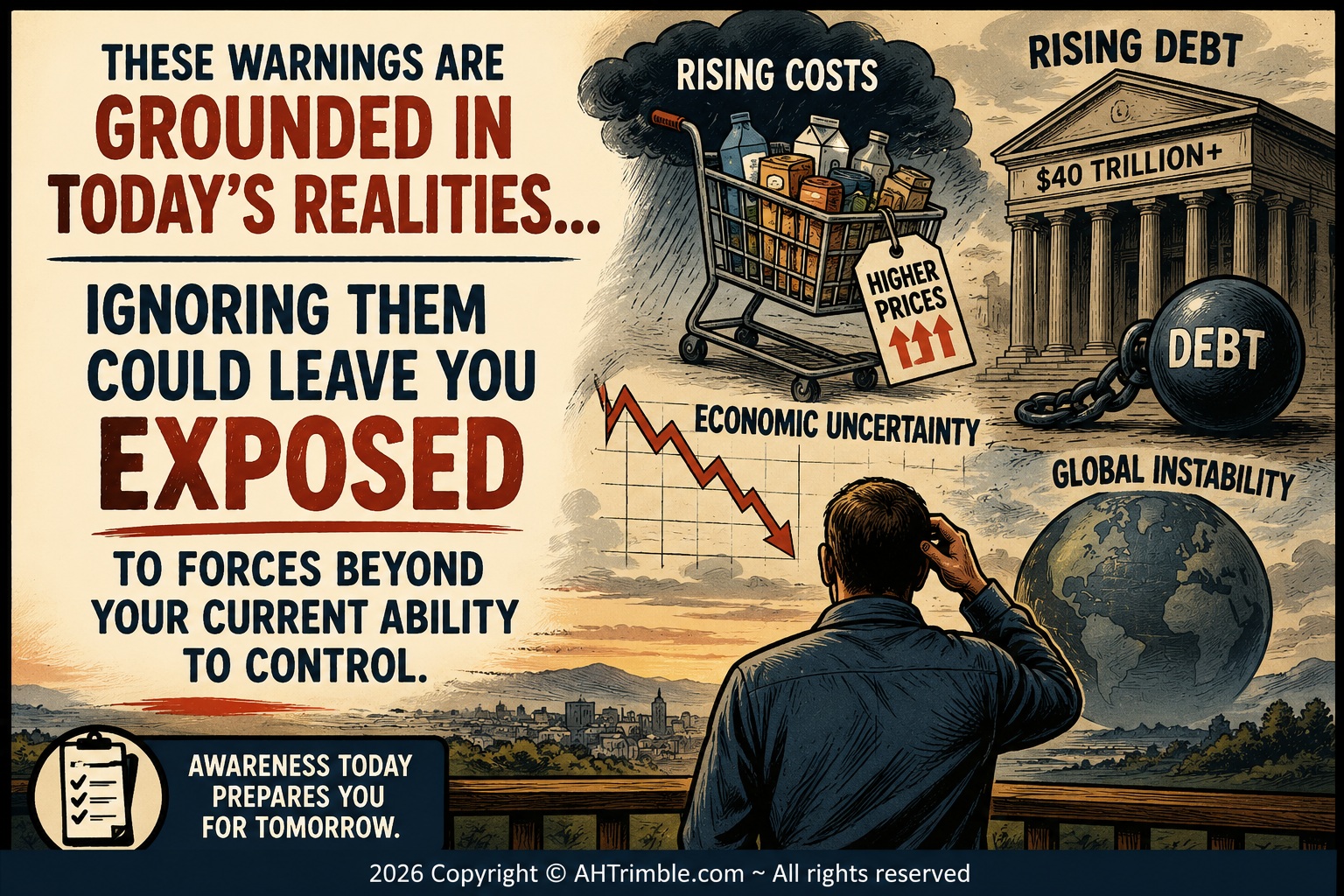

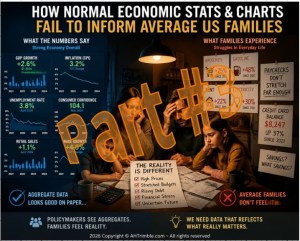

Let’s start with the obvious…lots of people already feel economically stressed, financially squeezed, uncertain, and distrustful. What many ordinary people lack is constructive and practical direction…simple steps they can begin taking today, tomorrow, and the next day to improve stability and prepare for an uncertain economic future.

There are two camps in the United States today. One screams, “Everything is rigged! Collapse is inevitable! Nothing can stop it!” The other quietly nods, “Everything is basically fine…this is normal…just keep on keeping on.” There there’s Ray Dalio and his extensive research on The Fall of the US Empire <click here to read that article >.

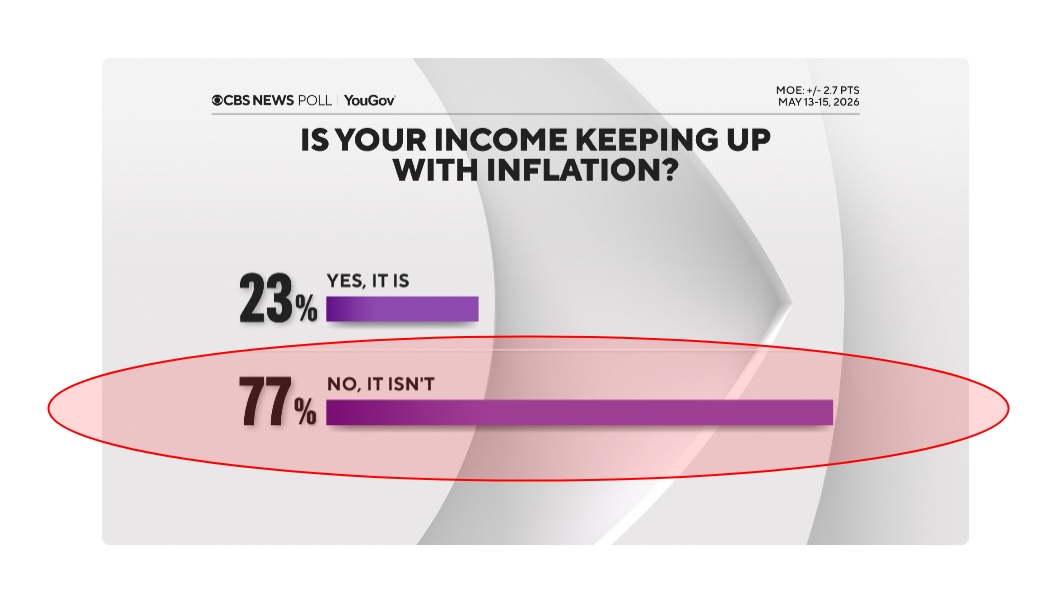

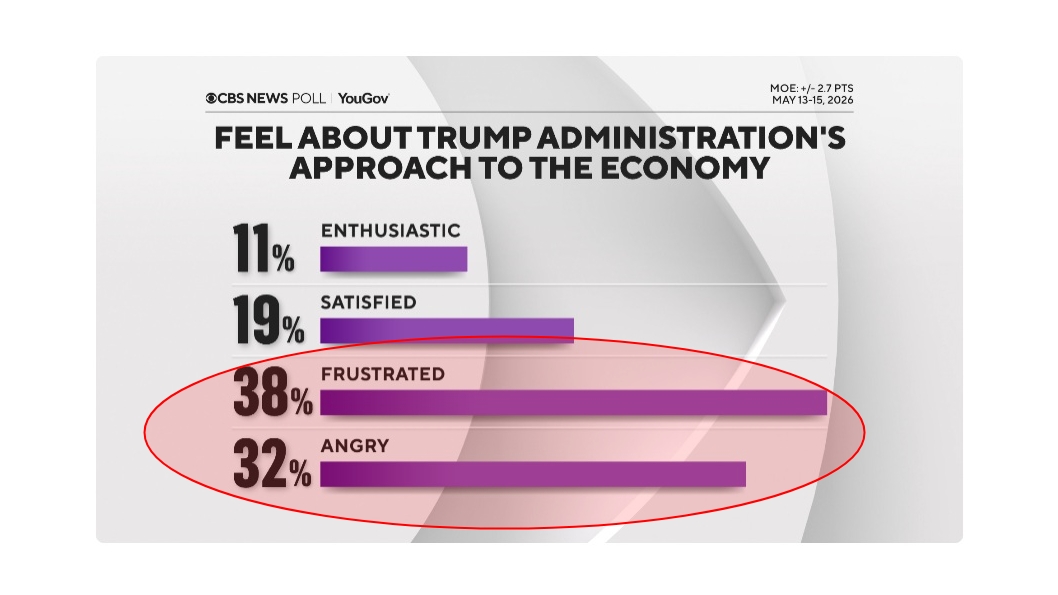

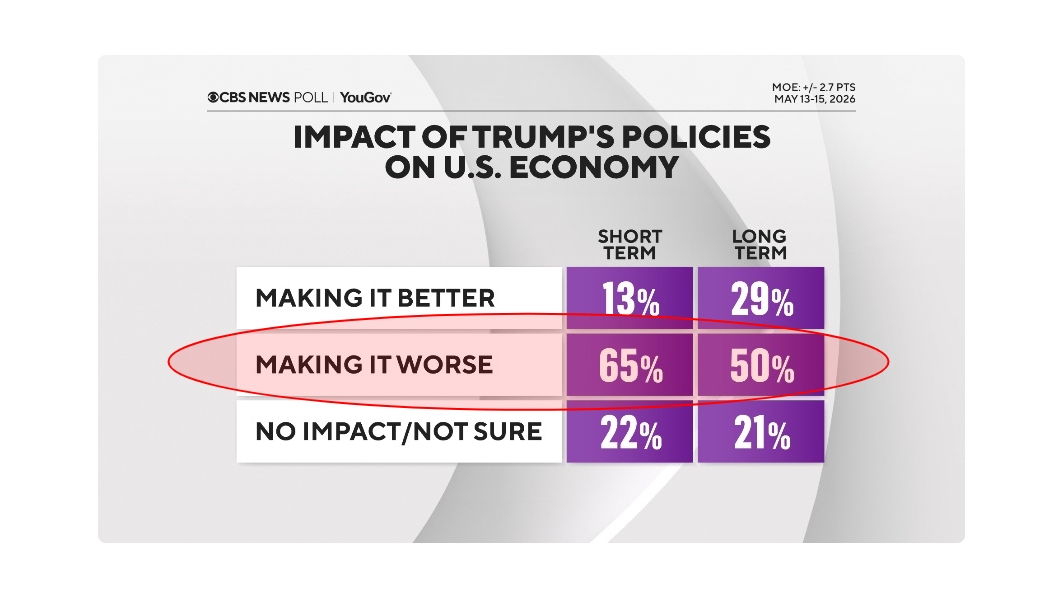

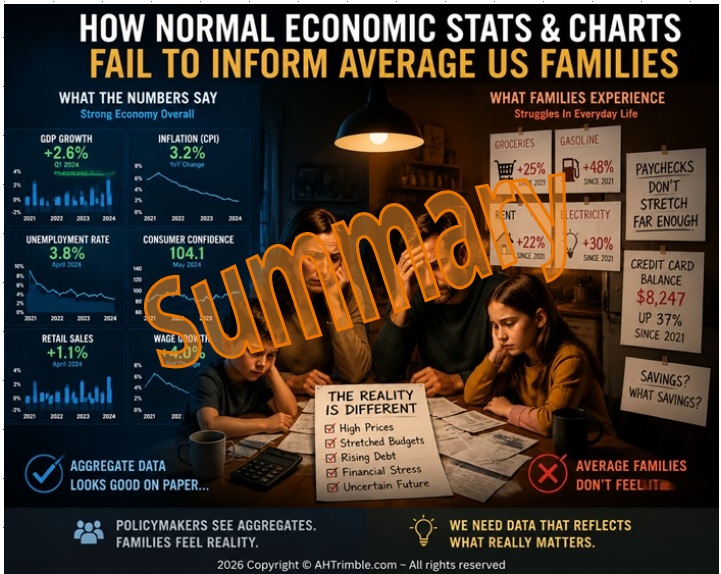

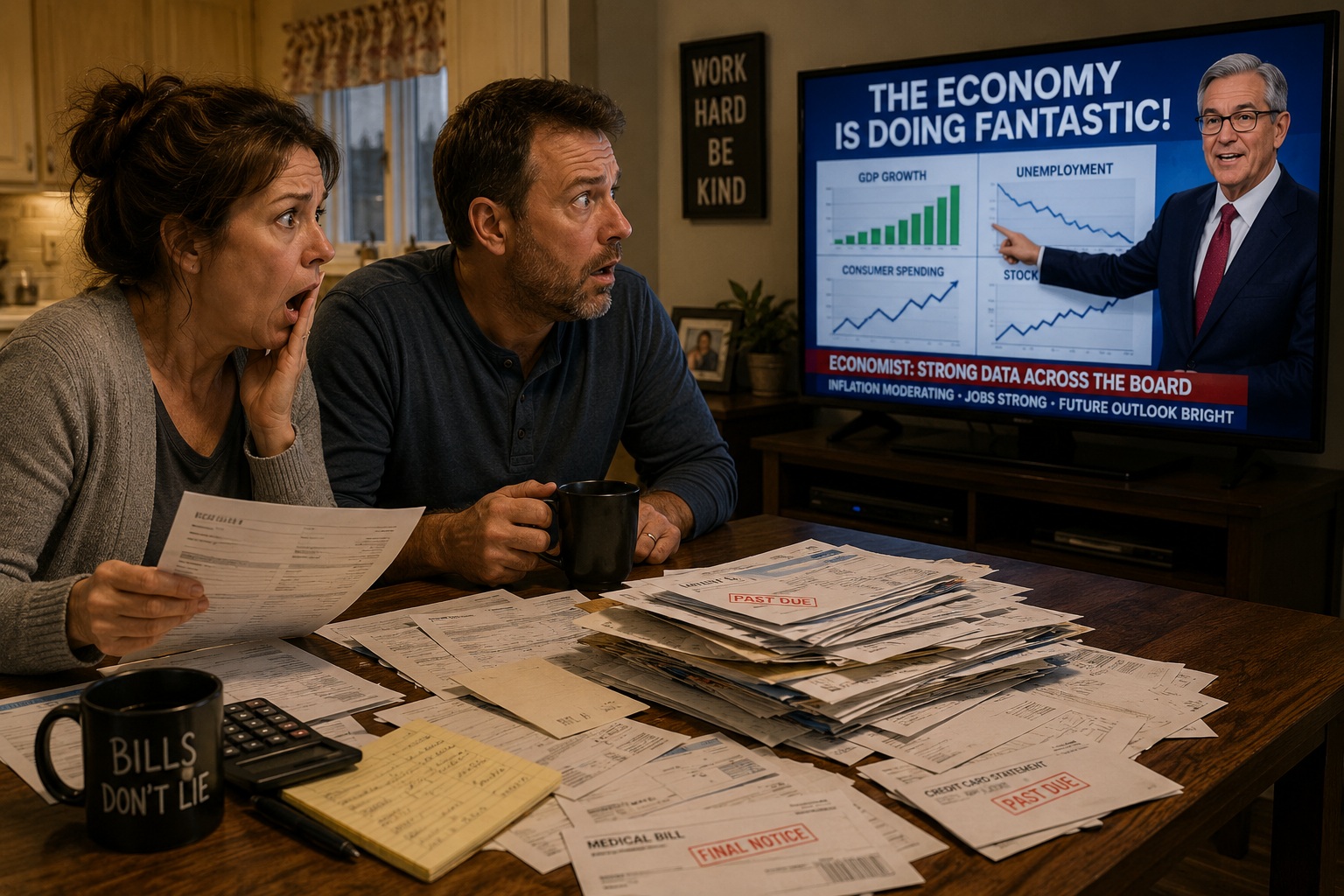

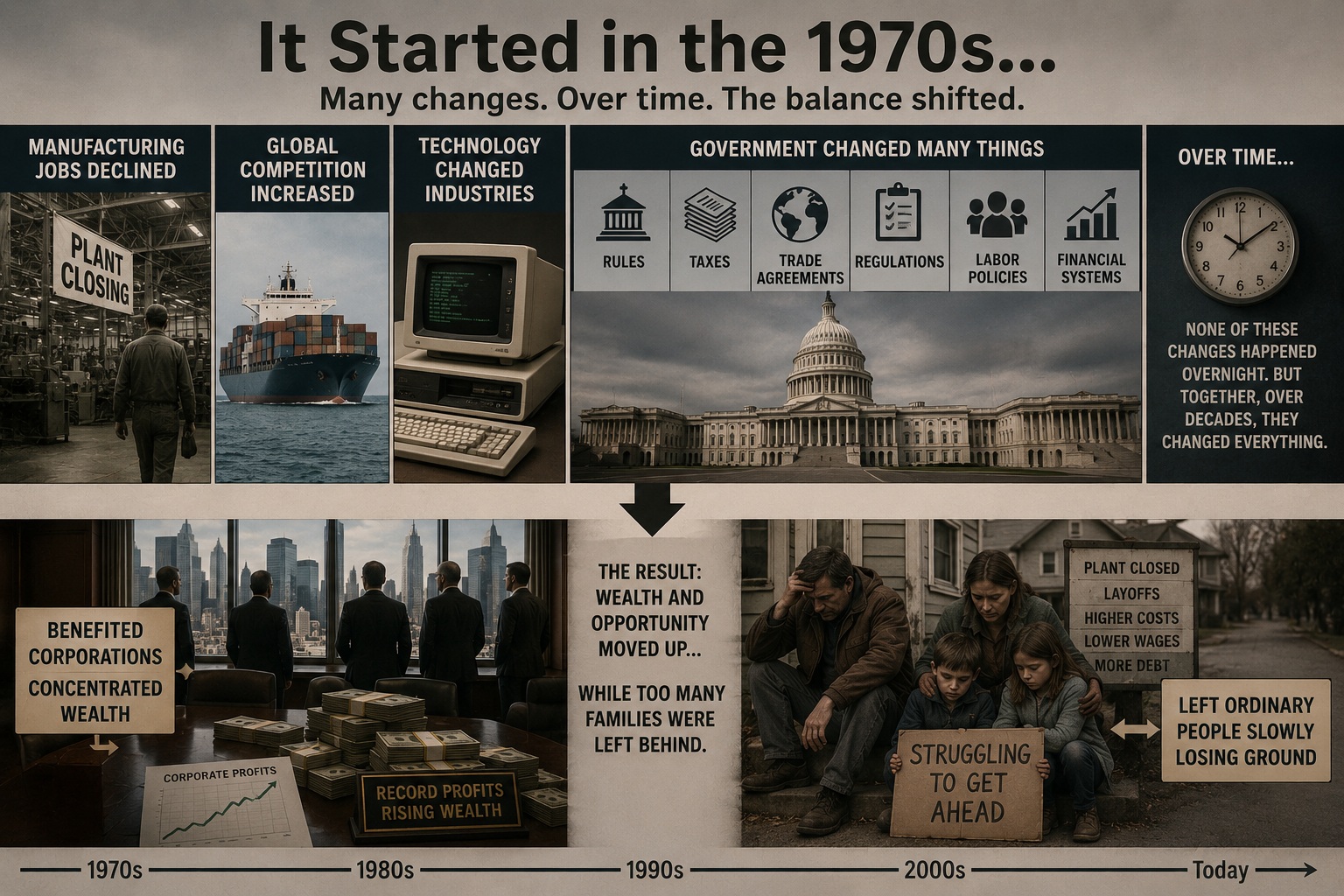

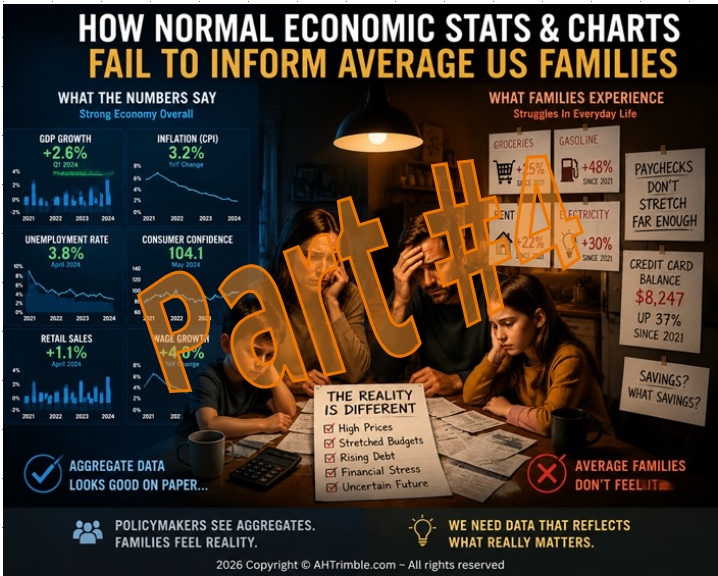

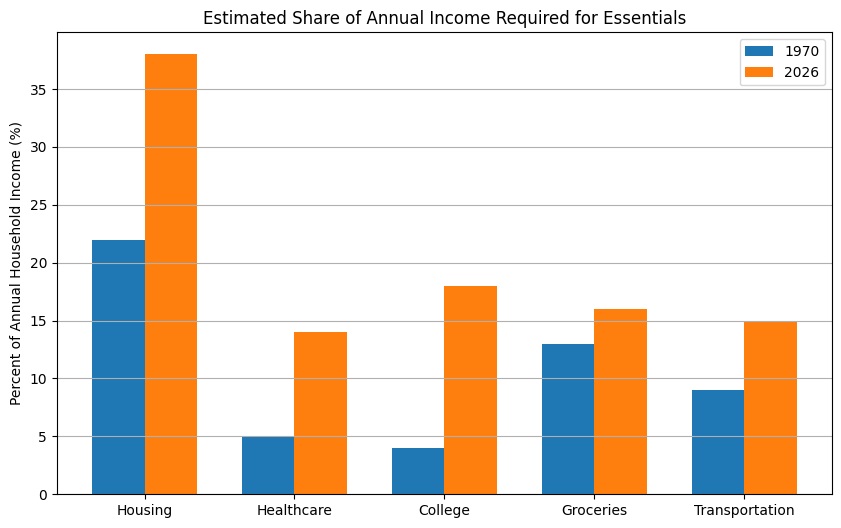

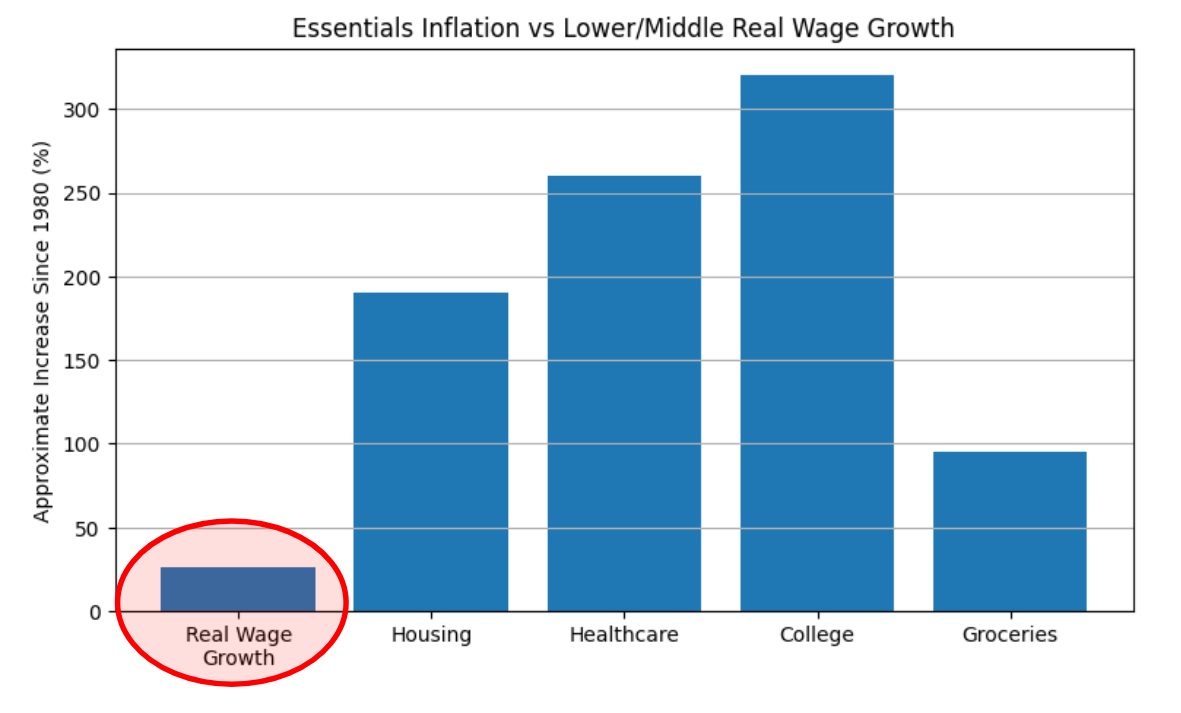

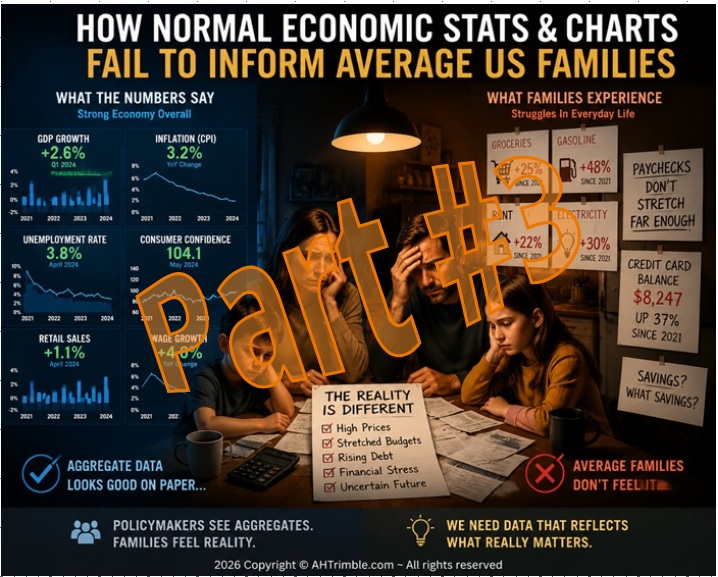

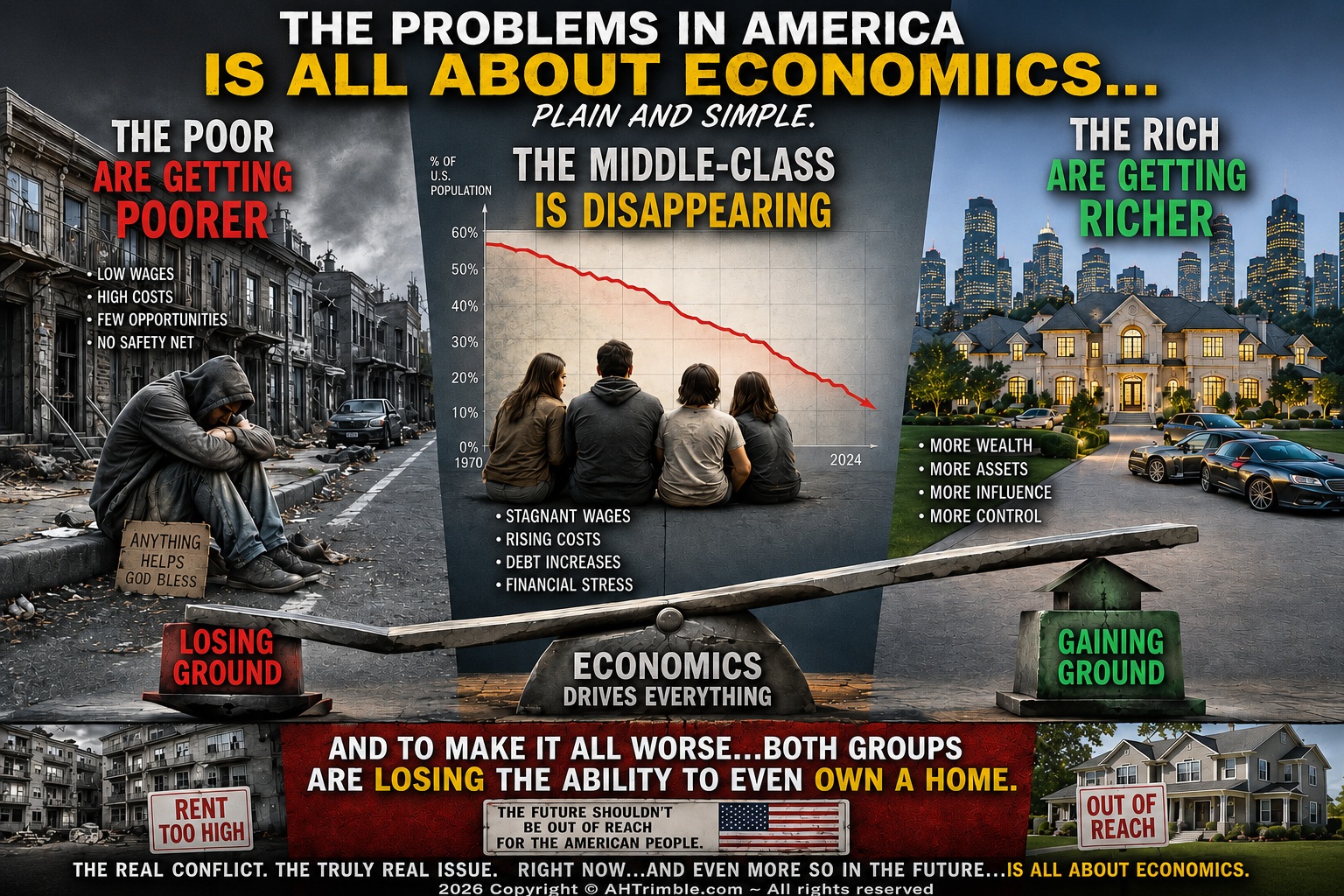

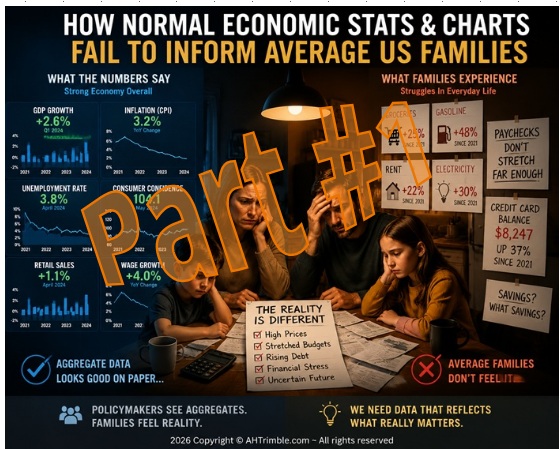

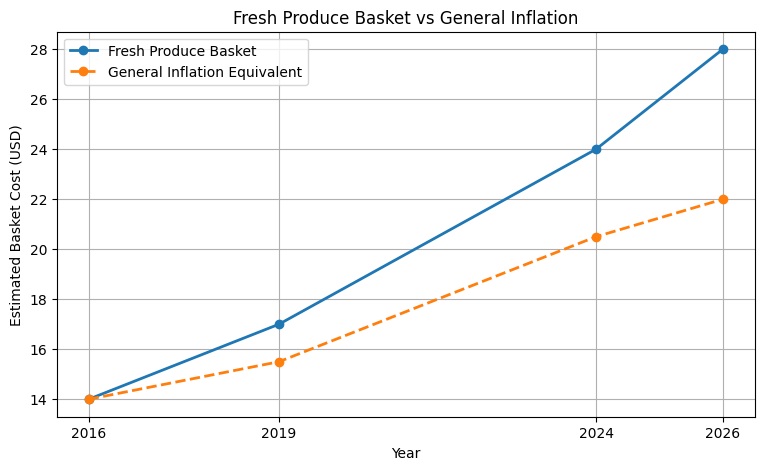

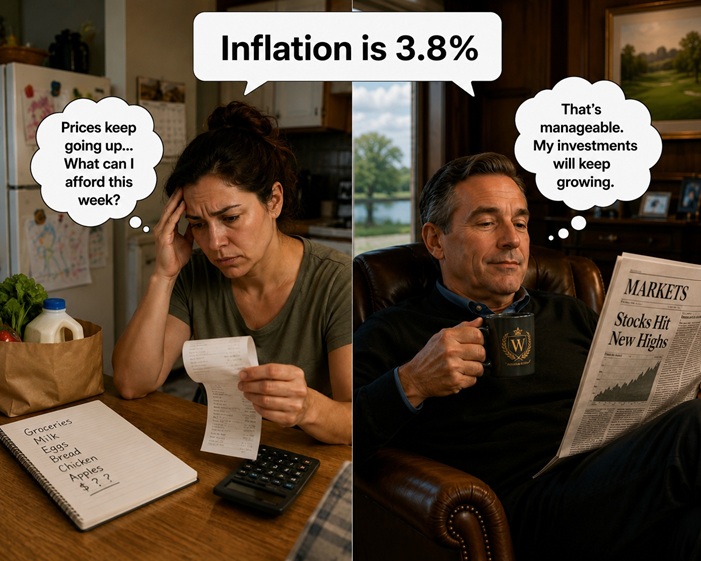

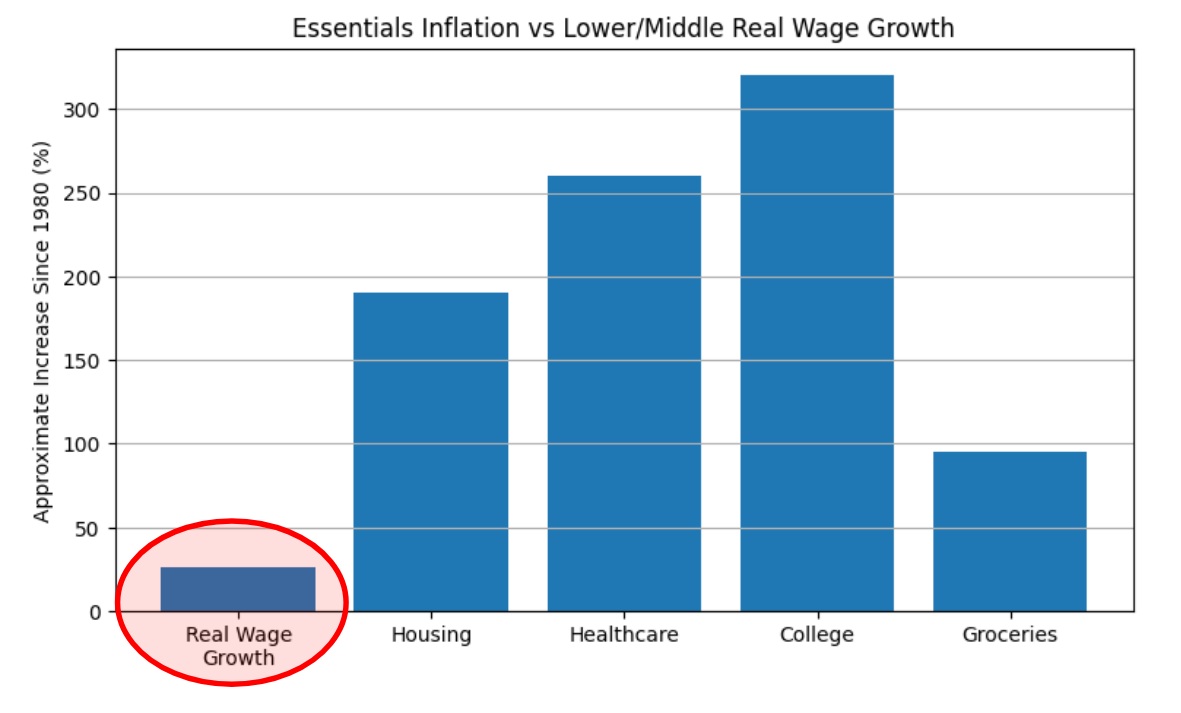

I get why both sides exist, but neither tells the full story. The truth is harsher but slightly more balanced…the system isn’t fine, and it isn’t collapsing tomorrow. The “system” is however, increasingly fragile…financially, socially, and politically speaking. Ordinary households are feeling it, day in and day out. Families are struggling to pay for essentials, buy a home, save for the future, or hold onto stability. This isn’t theory…it’s lived reality. This is our lives…our experience.

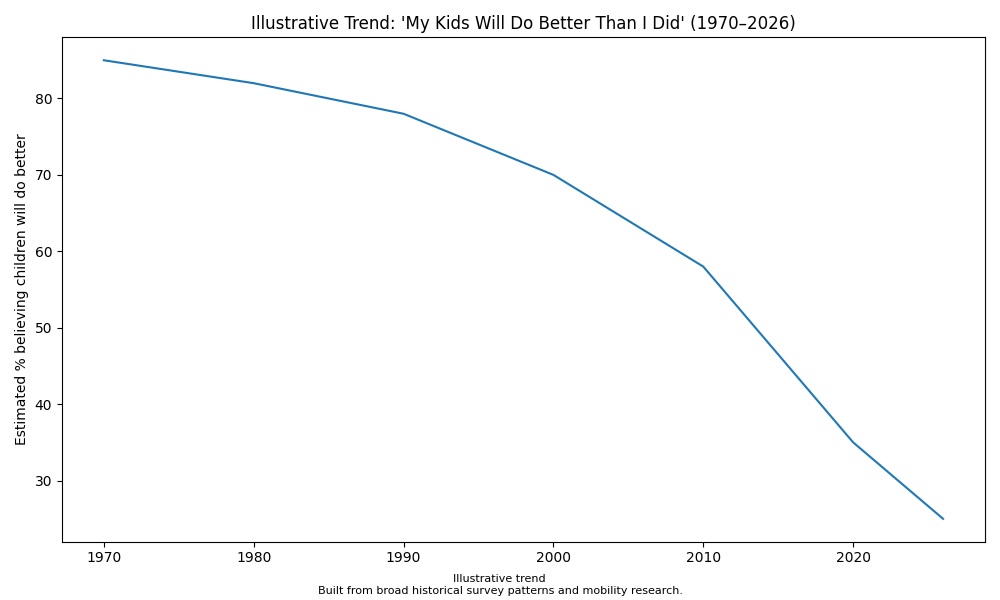

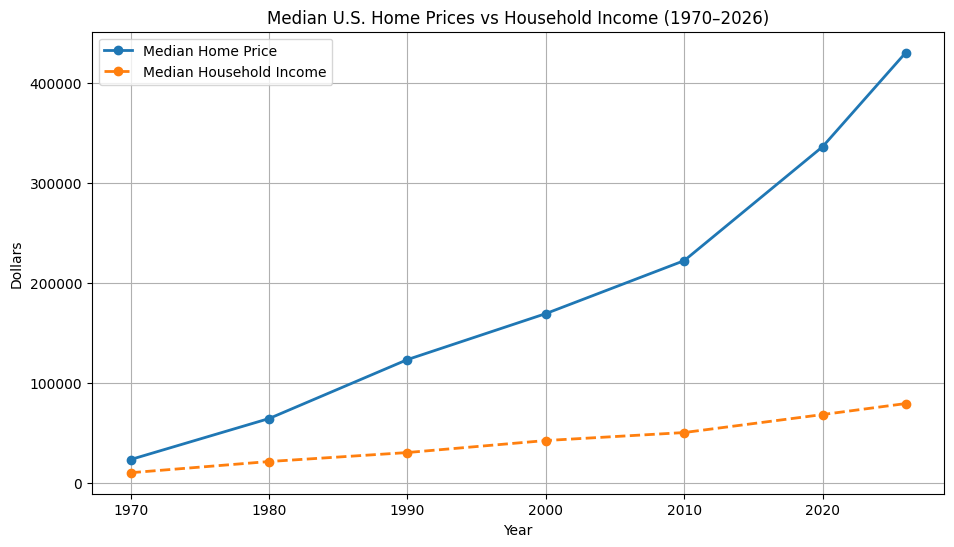

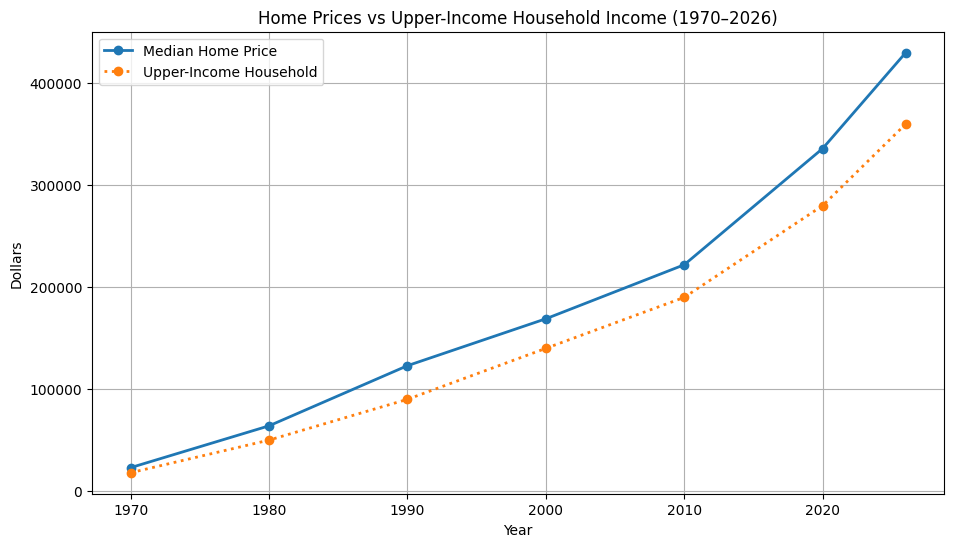

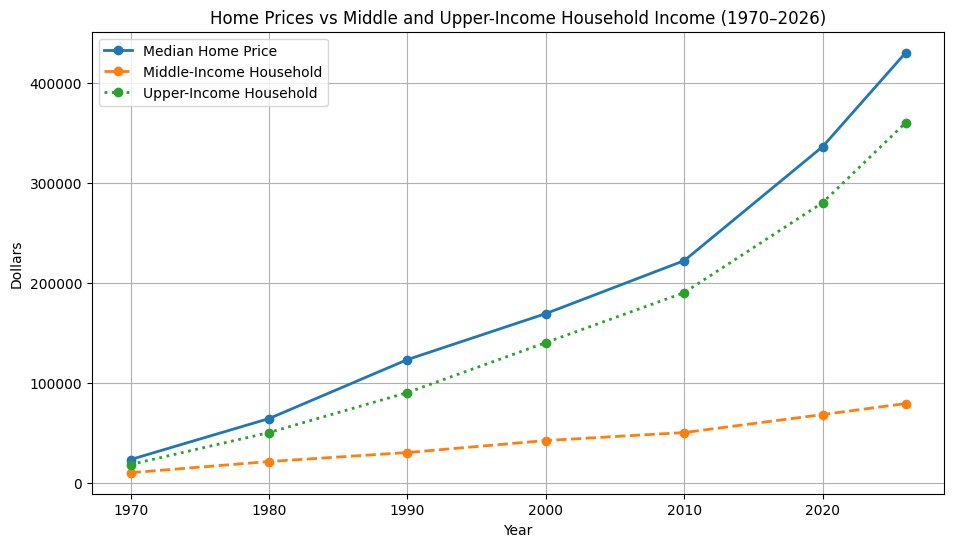

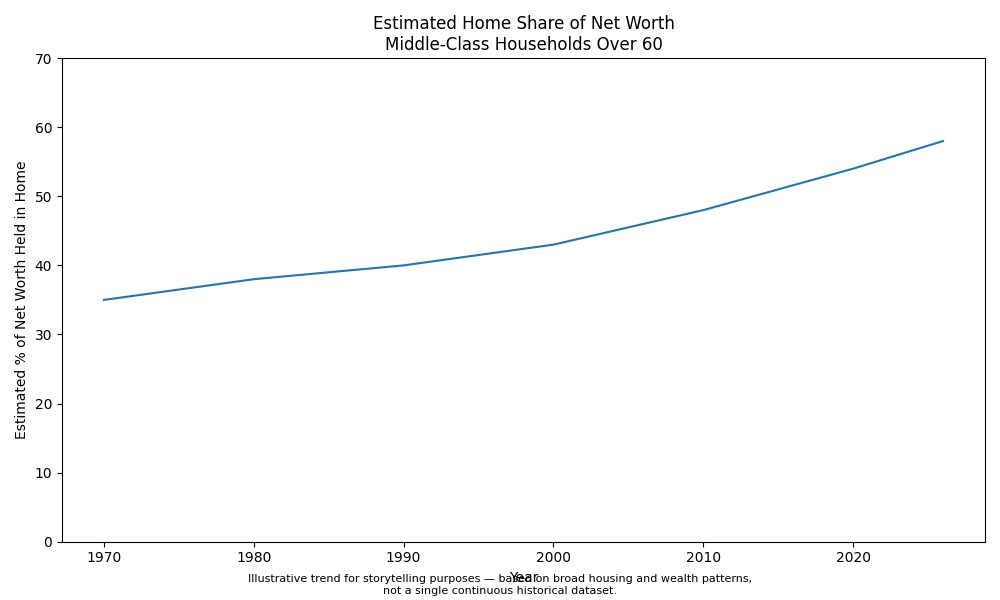

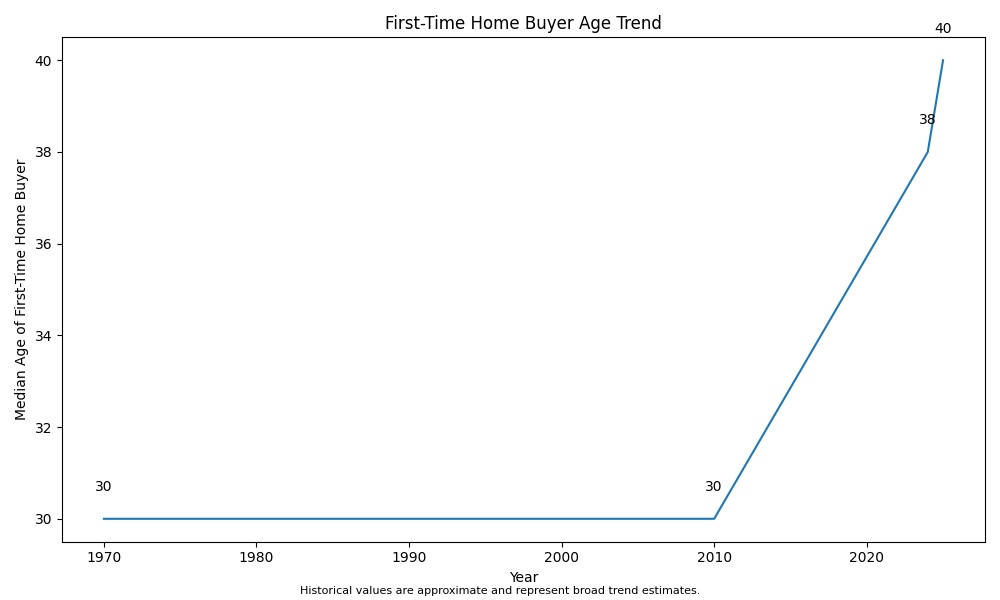

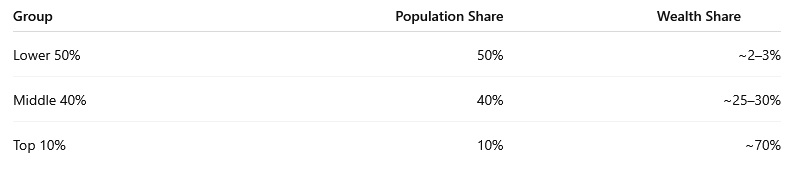

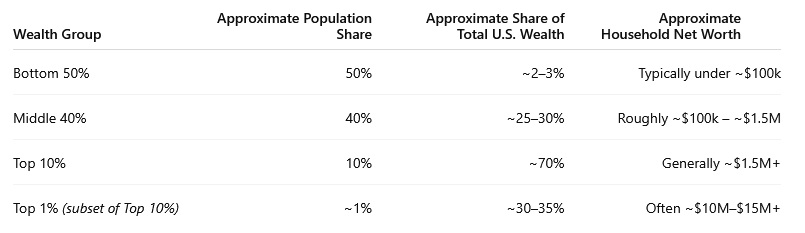

And here’s the worst part: most people don’t even see all of this yet…statistics show families are barely scraping by economically, while the system keeps stacking more weight on their shoulders. And while the rich continue to accumulate more wealth and influence, the crushing economic pressures on everyone else keeps growing. People aren’t just losing ground slowly; they’re losing real financial security and have been for 60 years. That’s why paying attention…and taking practical steps…is no longer optional…it’s about survival.

First off…from the heart, I truly believe the U.S. economy, as it is today, is already strained and failing. It hasn’t officially crashed, but it is clearly heading toward serious trouble…which could include a total crash/collapse. I also believe the economic system will have to change…and it will change. What I can’t say for sure is exactly what it will change into.

If I was writing this a year ago it would look like this…

If I was writing this a year ago it would look like this…

That said, there are three primary broad paths I see for the U.S.:

- Slow, painful, incremental change: Tough, uneven adjustments over decades that may slightly improve conditions for lower- and middle-income families. (Roughly 50% probability)

- Partial adaptation: The current system is tweaked, becoming somewhat more economically friendly, but ordinary households still face strain and instability. (About 35% probability)

- Major constructive restructuring: A broad, coordinated overhaul that stabilizes the middle class and creates real opportunities for the lower class. (Around 15% probability)

Technically, there are two outliers, a fourth and fifth possibility…both are much more extreme forms of changes/collapses that forces major change upon America. I won’t even try to assign a probability to them; there are simply too many  variables and potential outcomes to make a meaningful estimate. And if it is too extreme…it could lead to everything getting much worse…almost beyond comprehension.

variables and potential outcomes to make a meaningful estimate. And if it is too extreme…it could lead to everything getting much worse…almost beyond comprehension.

Outlier #1 – The economic disparity becomes so extreme and the lower & middle-class become so destitute, frustrated, or desperate that there is a revolution of sorts. It would be violent, bloody, and devastating to the United Stares…something that the US might never recover from. And the outcome is unpredictable at best.

Outlier #2 – Artificial Intelligence (AI) could begin to influence the economy in ways that are virtually unknown to us now. Massive job replacement creates unimaginable unemployment which would deform/devolve into an unknown size of residential displacement. Then the whole issue of how to put money into the hands of the massive numbers of newly unemployed so they can buy essentials such as food. One thing for sure…the lower & middle-class would morph into more of a single class of people…something worse than middle-class to be sure…but it is hard to properly and accurately describe at this point in time.

Breaking down the whole AI effect on the economy…AI can boost productivity while simultaneously reshaping jobs and income distribution, creating both opportunities but also challenges for the economy. The economic benefits will disproportionately go to companies and individuals who own AI systems and the company owners who use it…increasing wealth inequality if not “addressed.” Let me think about that one…when was the last time economic problems were “addressed” that benefited the lower & middle-class vs benefiting the upper-class? Well, we’ve seen in the last 60 years the economy has changed a lot…and made the rich WAY richer.

So those two outliers could seriously change the US economy in that would only hurt people not help people. Well, only hurt people who are not wealthy. But, that has been going for 60 years anyways.

Now, writing this today it looks like this…

- Rapid, painful and major change: Artificial Intelligence (AI) will begin to influence the economy in ways that are virtually unknown to us at this moment in time. Massive restructuring of employment. Large sectors of employment

will shrink rapidly, and that movement has already begun. Large corporations will continue to announce 10’s of thousands of jobs terminated with employees being laid off, retired, or terminated. Smaller companies will follow suit but in a less dramatic fashion. This will greatly burden already strained government assistance programs such as unemployment payments. Other sectors of the economy will be unable to absorb the massive job losses. The removal of salary and wages from the economy due to job terminations will begin to seriously affect consumer spending. Saving and retirement account withdrawals will disrupt stock markets and banking institutions. Federal government bailouts will strain federal budgets even more, federal deficit spending will increase along with the national debt. Companies who own, and to a more limited degree integrate, AI will see significant stock valuation increases and jumps in profitability. Conditions for low & middle-income families will continue the trend of worsening but at a more rapid pace. Wealthy investors in AI and related industries will see significant jumps in wealth and income. We will see the world’s first trillionaire. (50% probability)

will shrink rapidly, and that movement has already begun. Large corporations will continue to announce 10’s of thousands of jobs terminated with employees being laid off, retired, or terminated. Smaller companies will follow suit but in a less dramatic fashion. This will greatly burden already strained government assistance programs such as unemployment payments. Other sectors of the economy will be unable to absorb the massive job losses. The removal of salary and wages from the economy due to job terminations will begin to seriously affect consumer spending. Saving and retirement account withdrawals will disrupt stock markets and banking institutions. Federal government bailouts will strain federal budgets even more, federal deficit spending will increase along with the national debt. Companies who own, and to a more limited degree integrate, AI will see significant stock valuation increases and jumps in profitability. Conditions for low & middle-income families will continue the trend of worsening but at a more rapid pace. Wealthy investors in AI and related industries will see significant jumps in wealth and income. We will see the world’s first trillionaire. (50% probability)

- Noticeable change: The current system is tweaked in major ways at the federal government level by the Democratic Party in Congress and/or the Presidency, economic conditions become noticeably more economically friendly for ordinary households. But lower & middle-income families will still face growing economic strain and instability. (About 20% probability)

- Partial adaptation: The current system is tweaked in minor ways by the federal government, becoming no more economically friendly to lower & middle-income families in any noticeable way. Ordinary households will face increasing financial strain and instability while hearing reports about improving economic conditions. AI’s increasing influence will be slowed relative to #1 above but still steadily gaining influence in the economy. (About 20% probability)

- Major, rapid, and unexpected change: The economic disparity becomes so extreme and the lower & middle-class become so destitute, frustrated, or desperate that there is a revolution or civil war of one form or another. Such an event could be violent, bloody, and devastating to the United Stares…something that the US might never recover from. And the outcome is unpredictable at best. (About 10% probability)

That is how much the US economic situation has changed in just the last year.

Let’s touch on a “cousin” to economic problems…

This is a complex issue…The economy is already squeezing families. It’s hitting lower & middle-income households the hardest, and it is increasingly becoming more obvious that it’s spilling over into a “two-tier justice system,” tribalism, and increasing distrust of all institutions. That is roughly combined into what’s called “social fragmentation.”

Social fragmentation breeds weaker community bonds, erodes shared identity, creates more loneliness, less civic involvement, and an ever increasing “every person for themselves” mindset. Or it’s uglier sibling, the “us vs them” philosophy. Which is a form of tribalism…just two tribes viewing each other with distrust and disdain. Whatever the case, whichever the term…families and communities are increasingly strained because of debt, housing stress, healthcare costs, rising daily essentials costs, and wealth concentration…on top of that is intensifying political polarization.

Social fragmentation breeds weaker community bonds, erodes shared identity, creates more loneliness, less civic involvement, and an ever increasing “every person for themselves” mindset. Or it’s uglier sibling, the “us vs them” philosophy. Which is a form of tribalism…just two tribes viewing each other with distrust and disdain. Whatever the case, whichever the term…families and communities are increasingly strained because of debt, housing stress, healthcare costs, rising daily essentials costs, and wealth concentration…on top of that is intensifying political polarization.

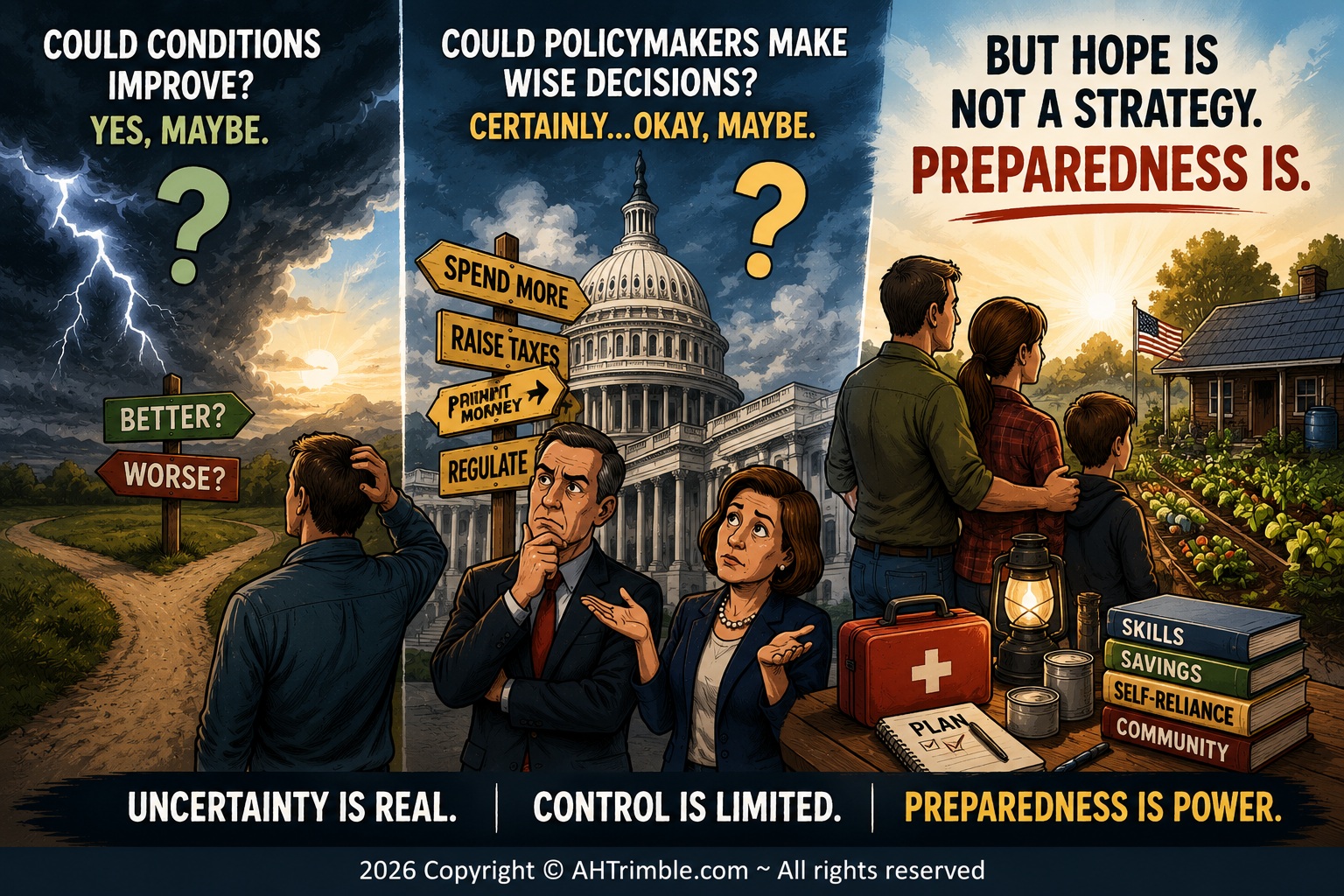

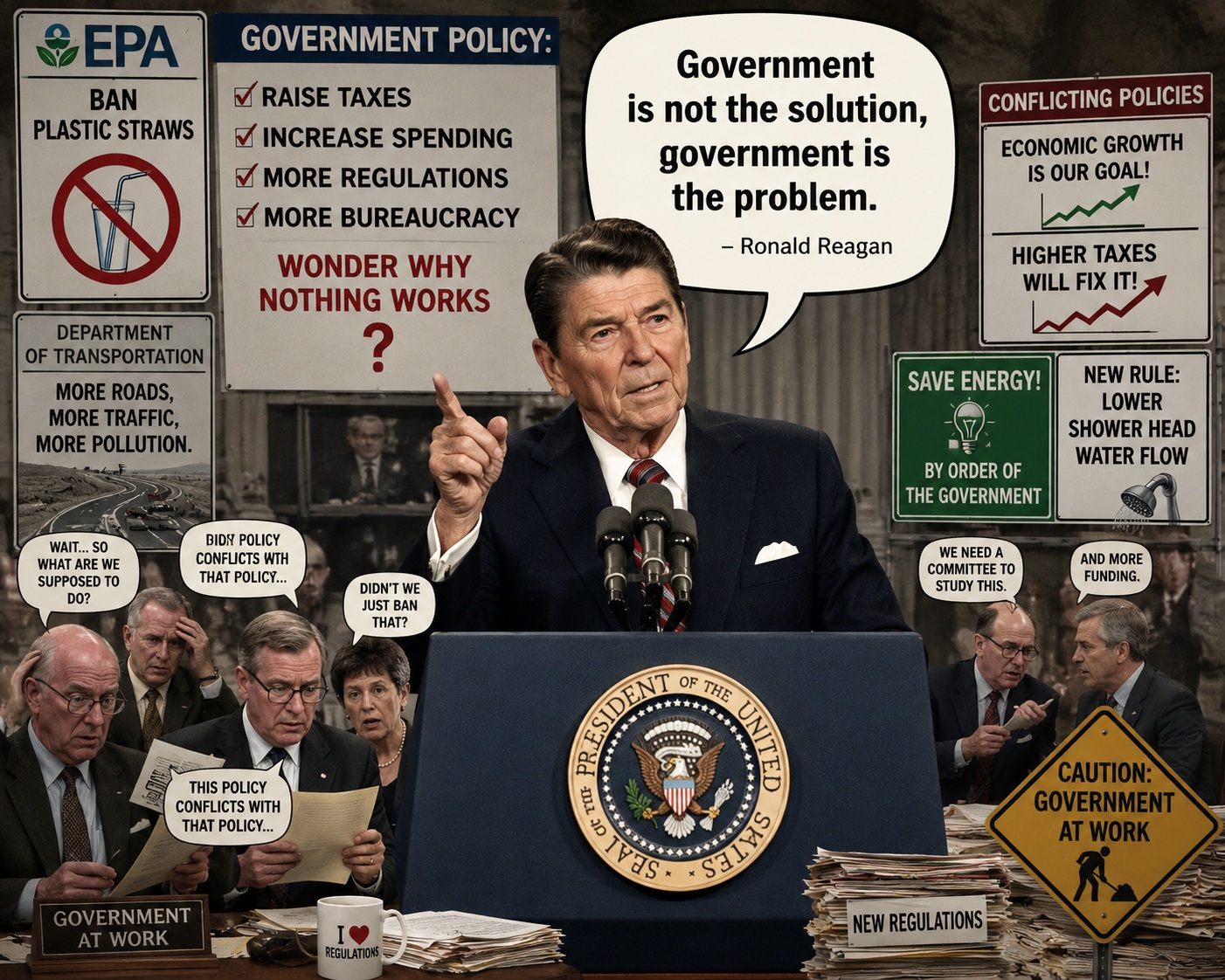

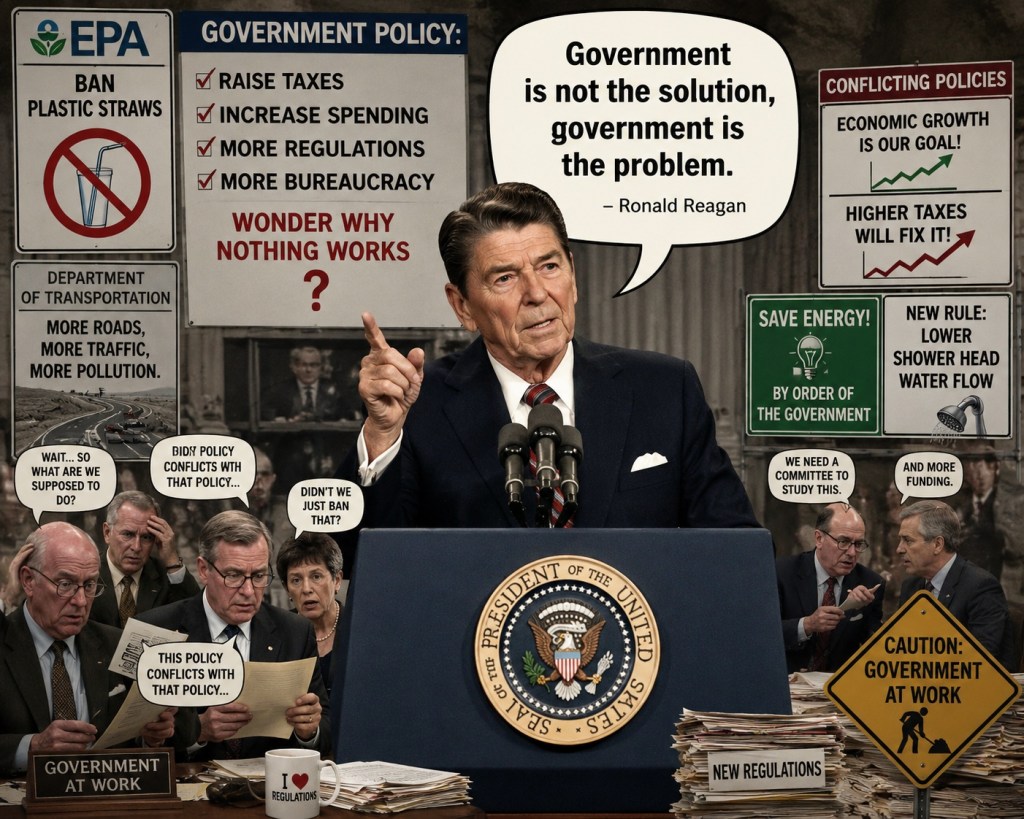

Historically, governments try to “fix” these problems with regulations, tax changes, labor policy tweaks, safety nets, shifts in industrial policy, or other governmental interventions. And yet…how often does government really solve the problems? As Ronald Reagan said perfectly 45 years ago, “Government is not the solution, government is the problem.”

For the sake of your family, I do not believe we can sit back and rely on government, government at any level, to fix this. Too often governments create solutions that bring unintended consequences, and even their best efforts can sometimes make things worse. Maybe we’ve spent decades arguing over which gear in the machine broke while families were standing beside the machine trying to figure out why life felt harder.

For the sake of your family, I do not believe we can sit back and rely on government, government at any level, to fix this. Too often governments create solutions that bring unintended consequences, and even their best efforts can sometimes make things worse. Maybe we’ve spent decades arguing over which gear in the machine broke while families were standing beside the machine trying to figure out why life felt harder.

So now what? Would you like a few ideas on what to do? You know…some practical steps to take that can help.

Look at it like a giant buffet…a lot to choose from…some or all of it might apply to your situation. Proceed with those items that apply to you…and do so in a priority order (we’ll talk more about that later). Here are some concrete actions to consider:

- Clarify your principles and values — make sure your decisions align with what truly matters to your family.

- Reduce personal debt — pay down what you can, avoid unnecessary borrowing.

- Live within your means — spend thoughtfully, avoid impulse purchases.

- Learn practical skills — first aid, basic home defense, trades, DIY projects.

- Food security — grow a garden, store essential staples, buy locally when possible.

- Strengthen your community networks — neighbors, churches, clubs, local groups for mutual support.

- Diversify skills and income — develop multiple ways to provide for yourself and your family.

- Practice self-reliance in everyday life — repair, build, and maintain what you can instead of relying entirely on outside services.

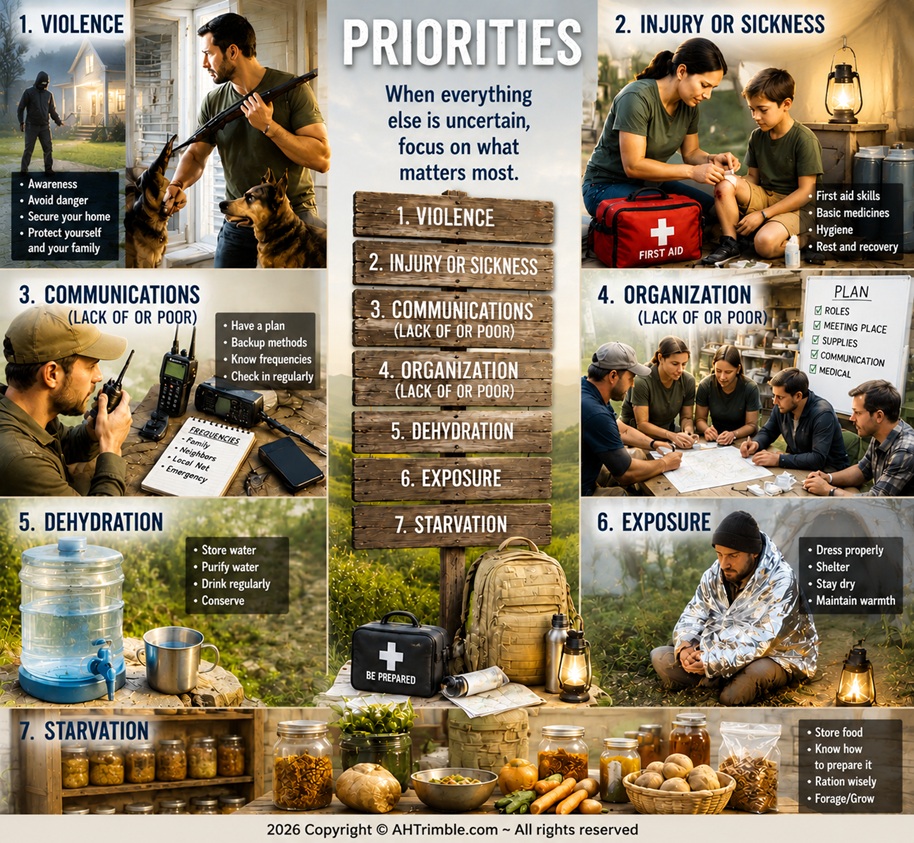

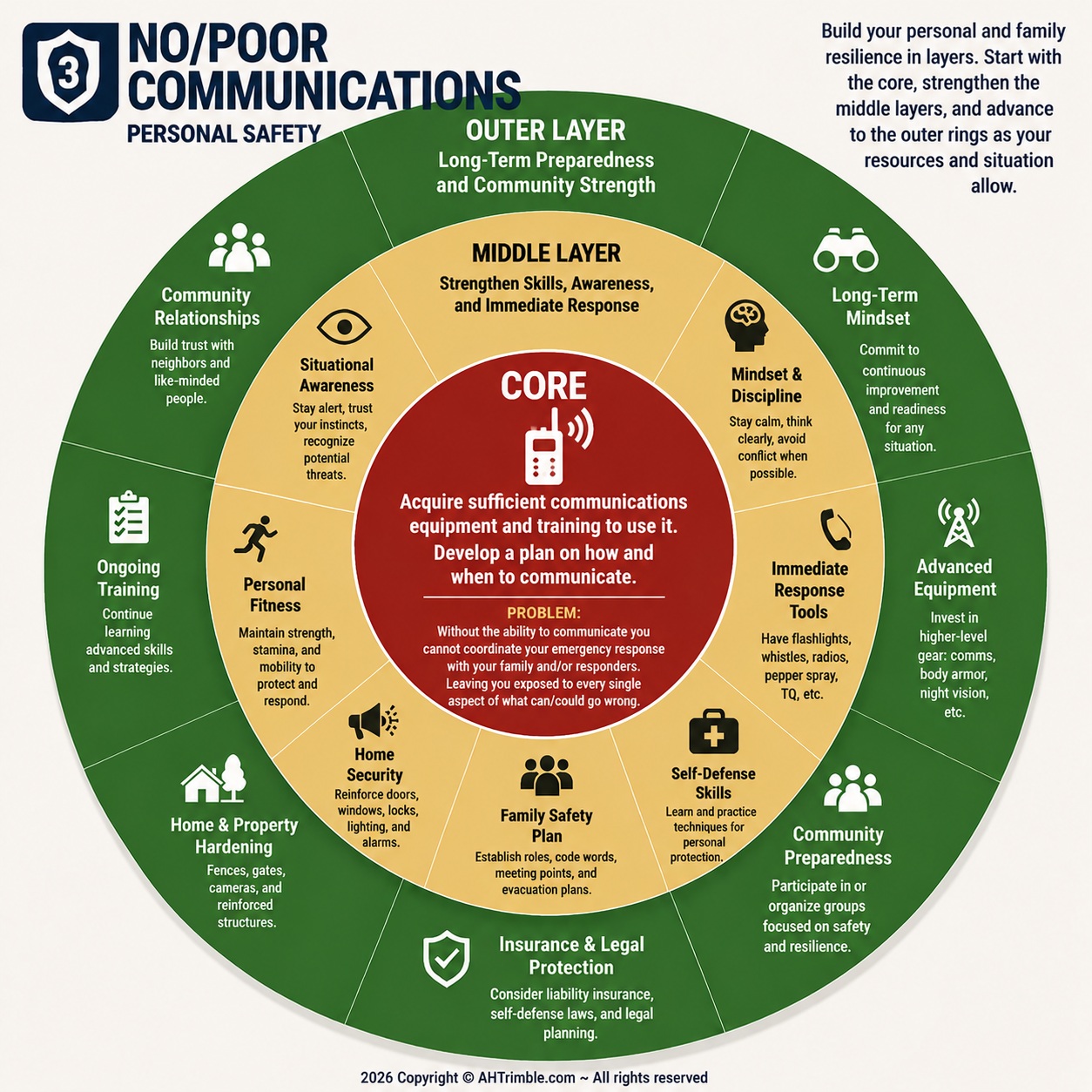

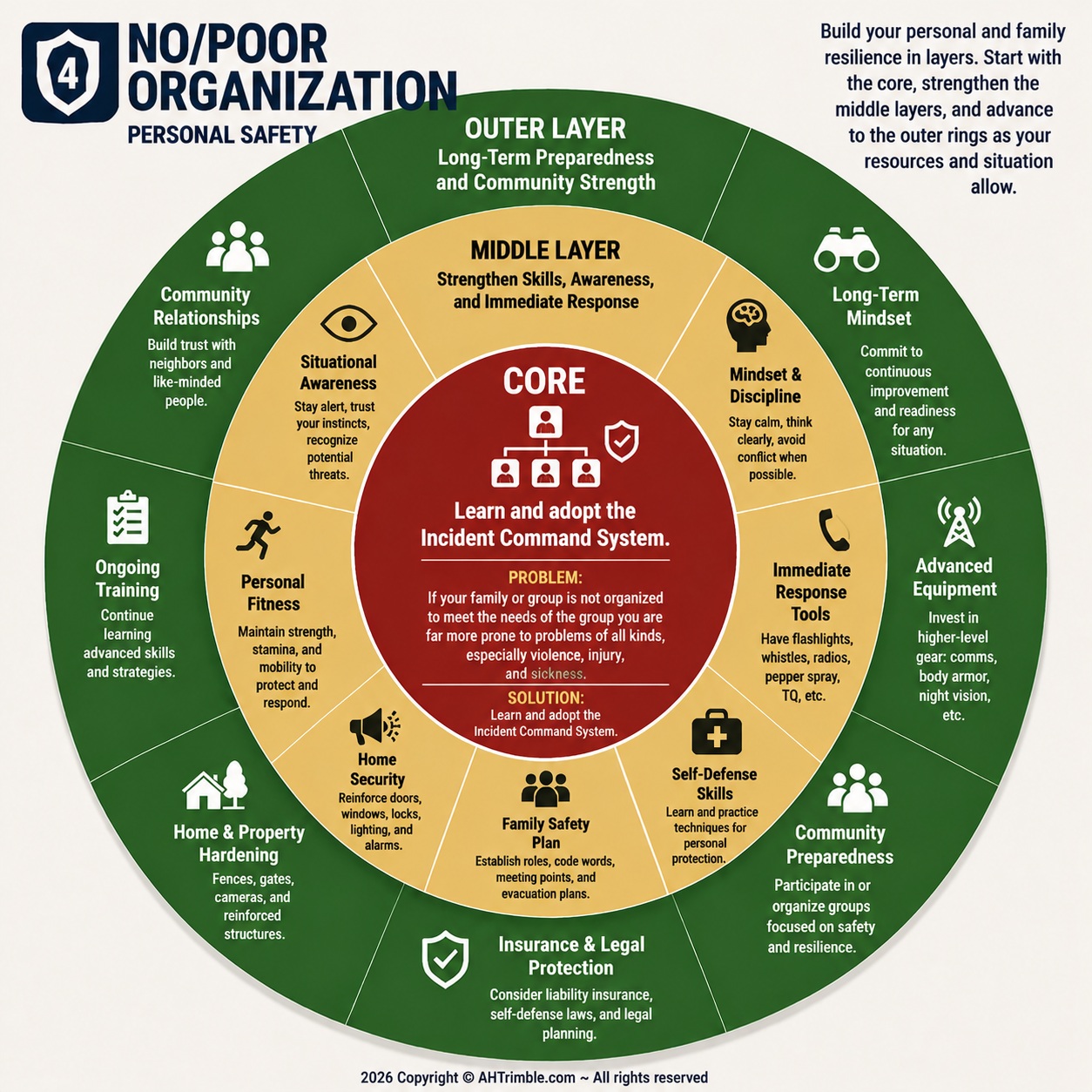

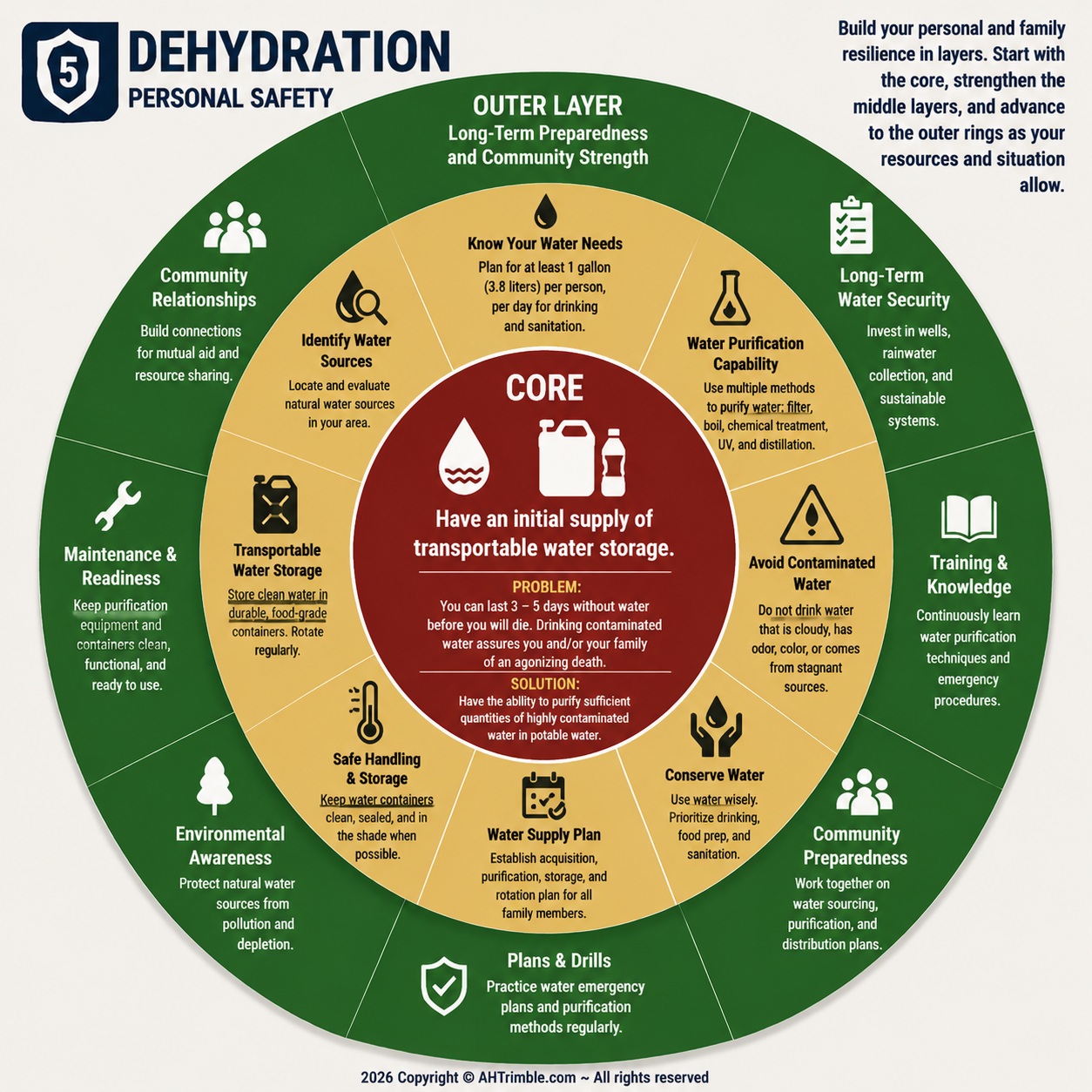

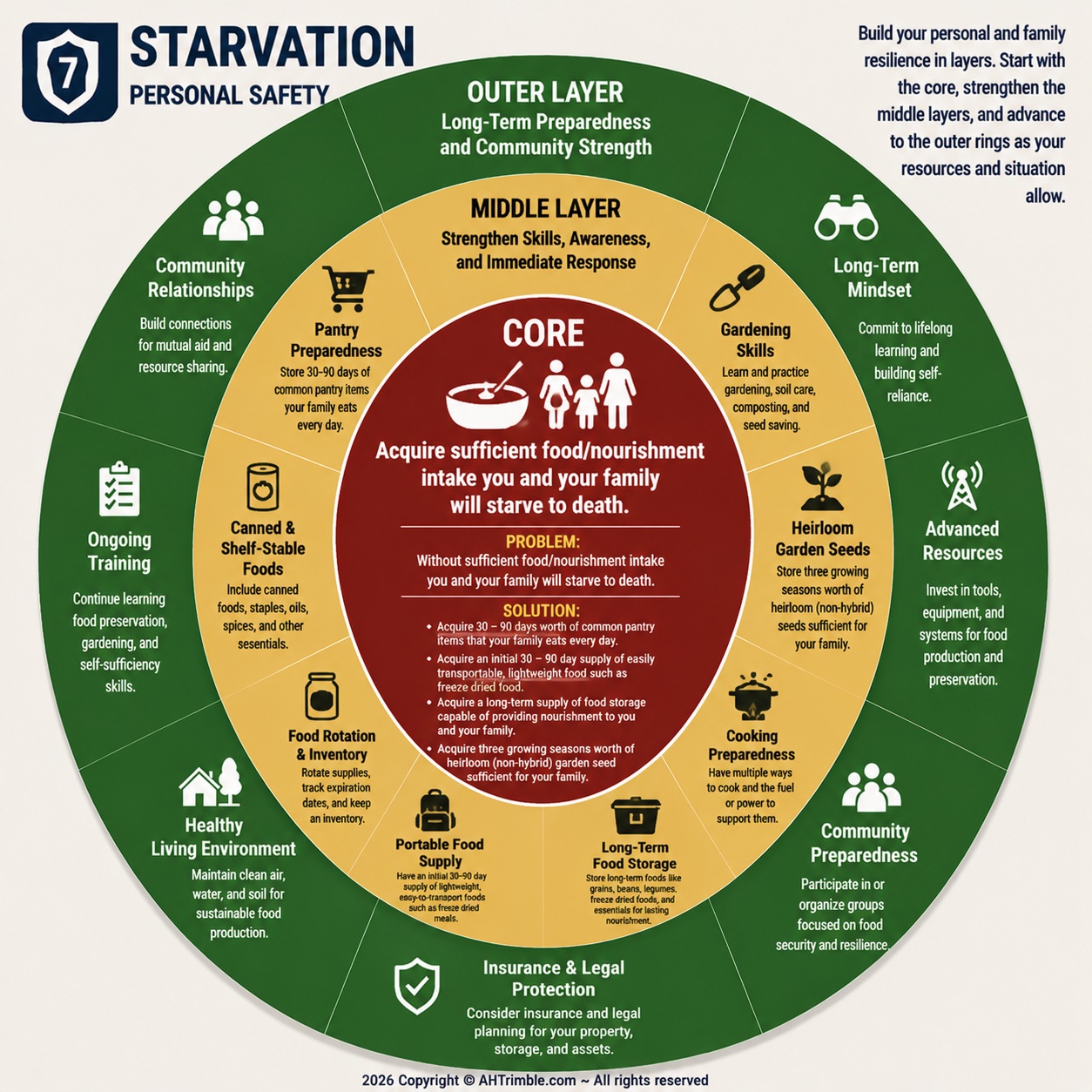

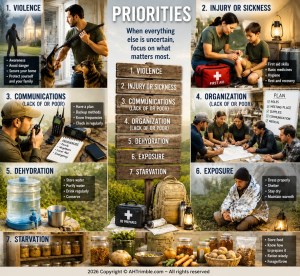

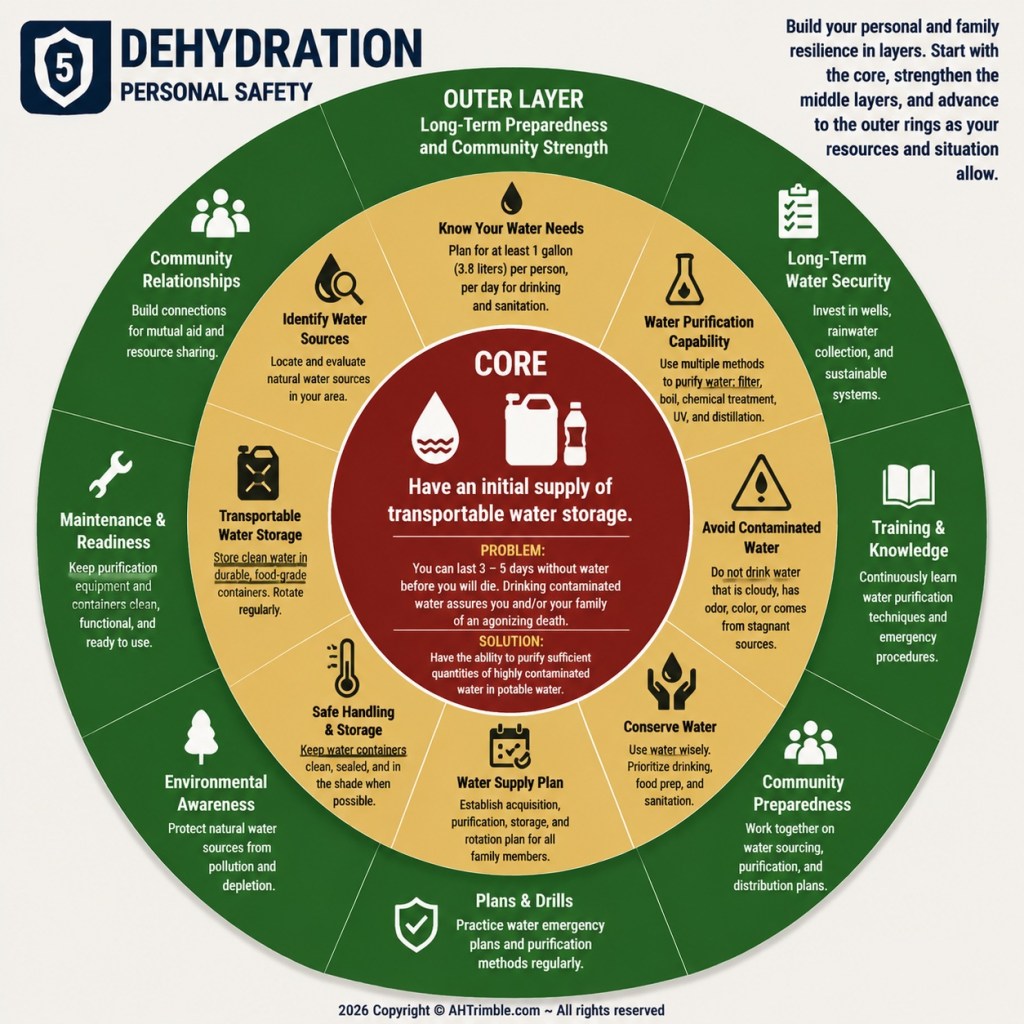

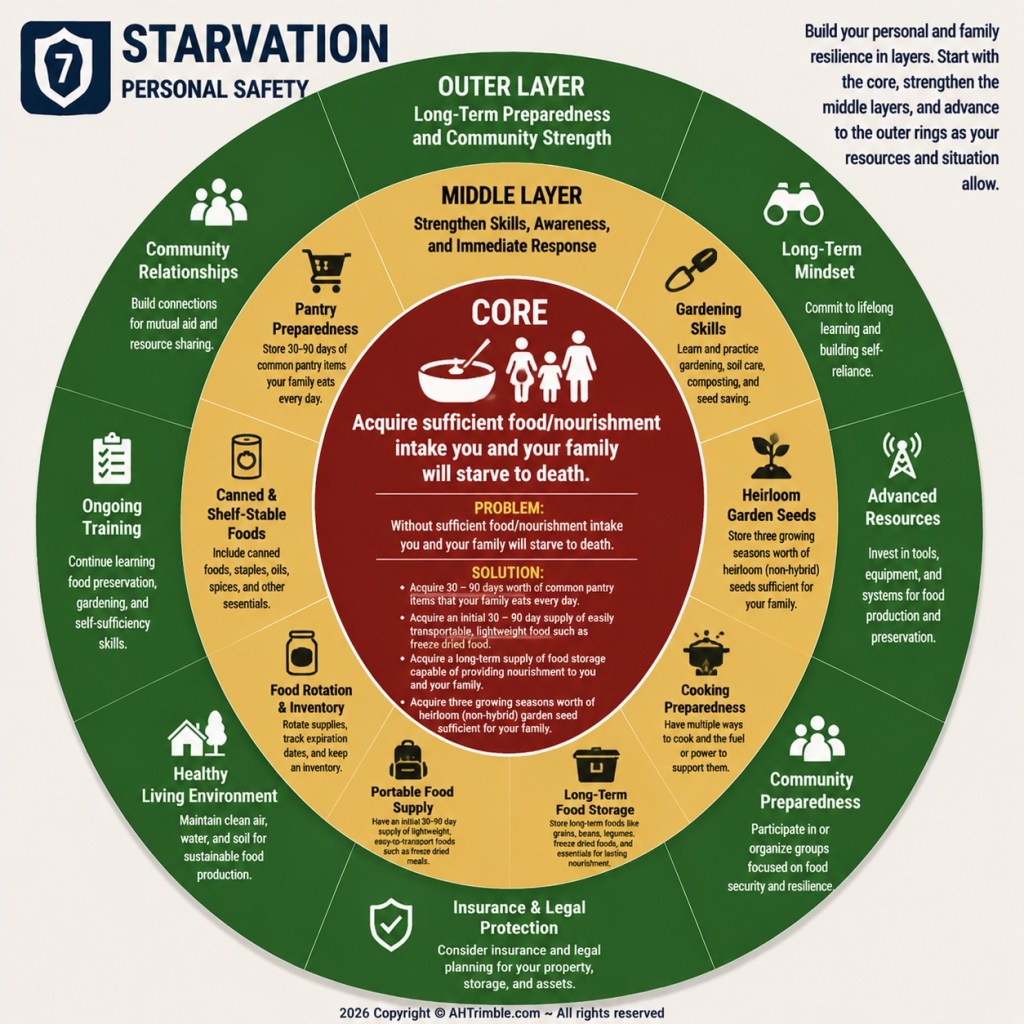

Now…”priorities”…Here is the list of the most common risks/threats to emergency, disaster, and grid-down situations; and they are in priority order.

Now…”priorities”…Here is the list of the most common risks/threats to emergency, disaster, and grid-down situations; and they are in priority order.

Consider them for just a minute…

- Violence

- Injury or Sickness

- Communications (lack of or poor)

- Organization (lack of or poor)

- Dehydration

- Exposure

- Starvation

You can look at today’s economic and overall situation in a similar way…but maybe not the urgency of a true emergency or disaster. Look at it more like a thought process to consider…”What can I work on first that prepares my family for pretty much anything?”

More help may be worth you reading about priority setting…L.I.P.S. < click here > Here’s the short version…

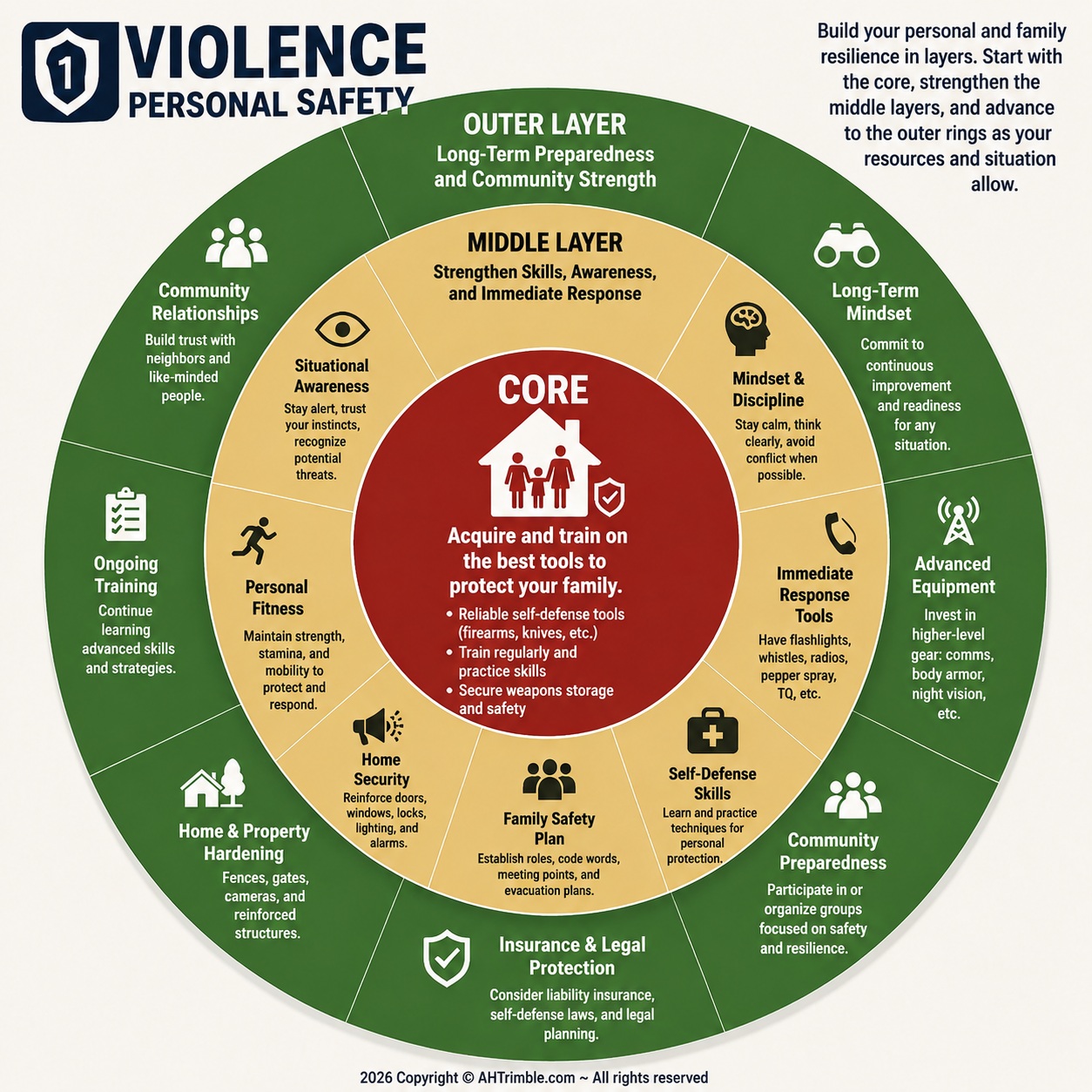

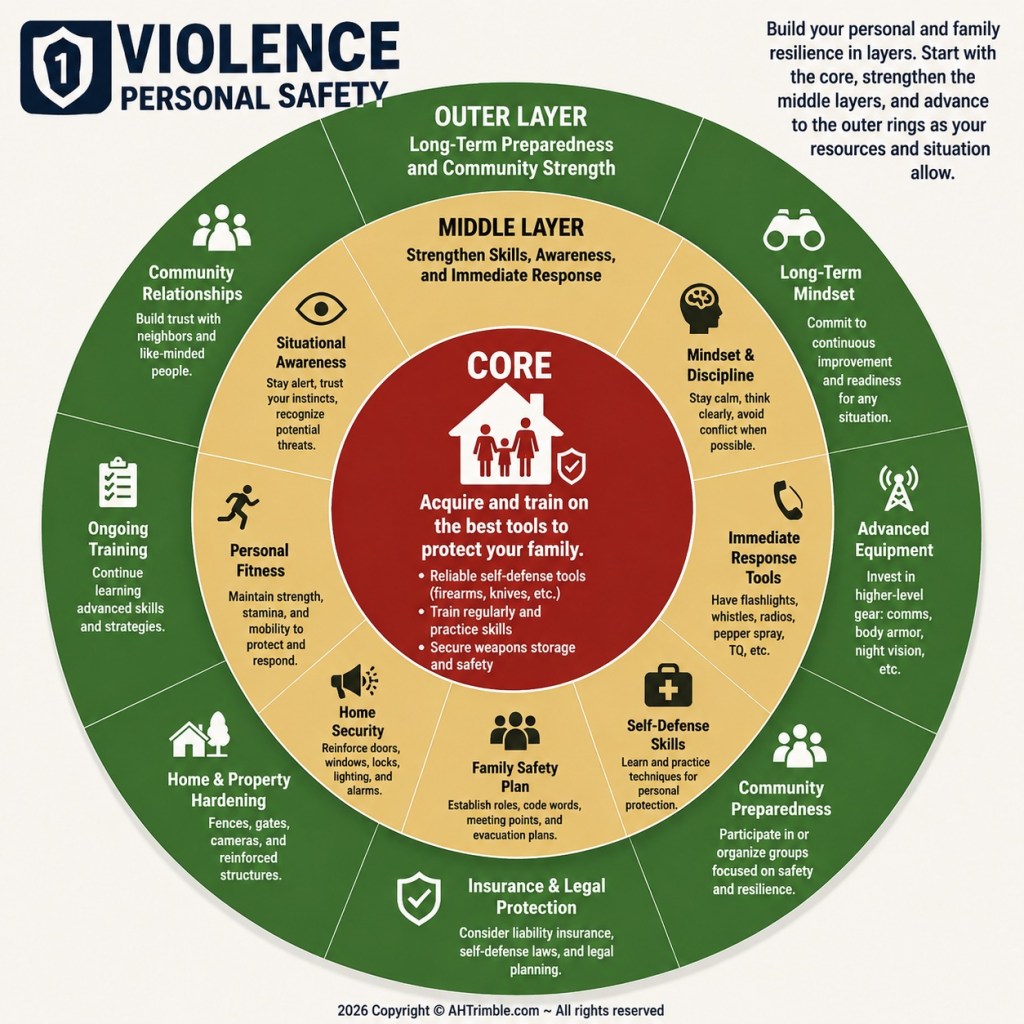

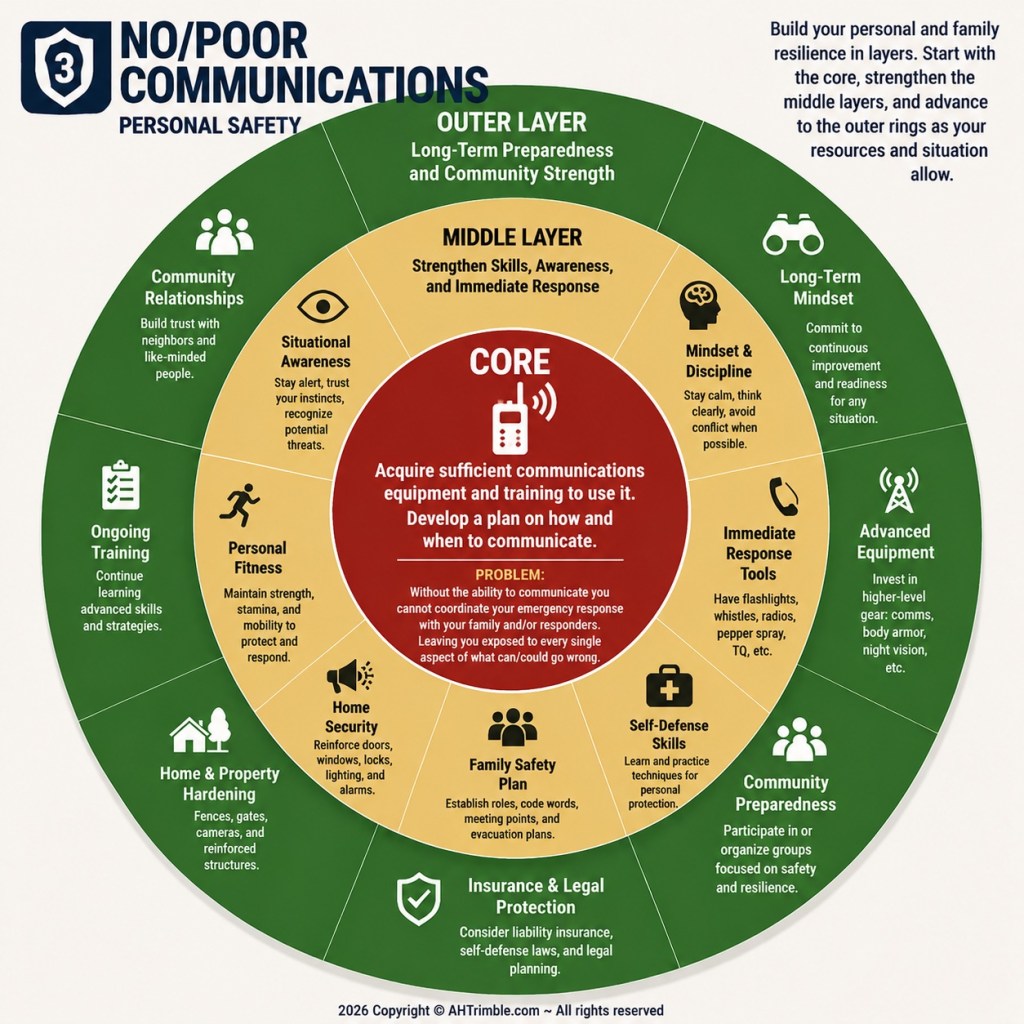

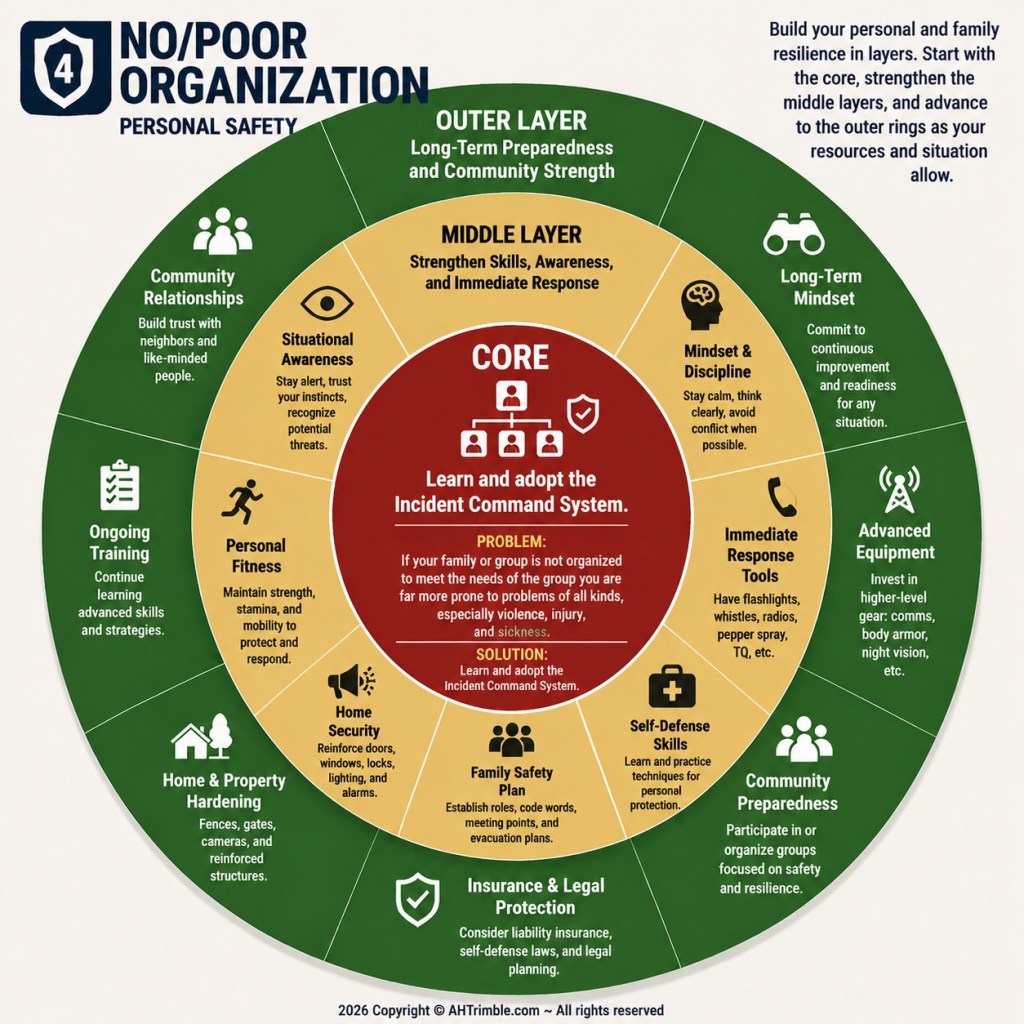

Let’s look at some things to do that can make you and your family more resilient. No long boring rambling text…just some cool info-graphics you can use for reference…

Let’s look at some things to do that can make you and your family more resilient. No long boring rambling text…just some cool info-graphics you can use for reference…

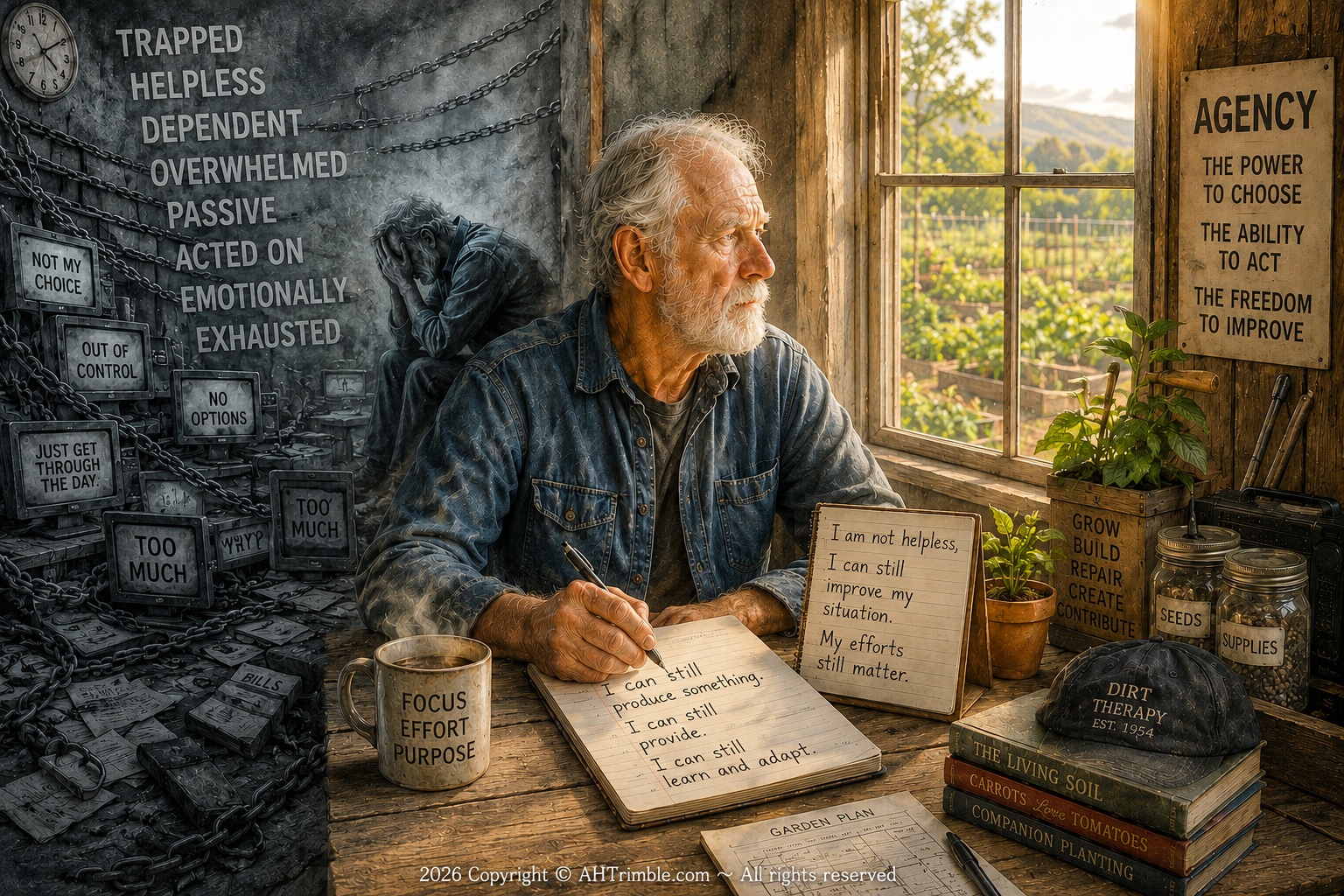

So there are answers to our awful economic situation…most of them start and end with us…as individuals. We, you and I, can take back control. Along with our neighbors, our communities, our congregations…we can once again become what we were made to be.

So there are answers to our awful economic situation…most of them start and end with us…as individuals. We, you and I, can take back control. Along with our neighbors, our communities, our congregations…we can once again become what we were made to be.

Tomorrow I’ll talk about regaining control and restoring agency.

← click here to read Part #2 Click here to read Part #4 →

Articles in this Series –

Related Articles –

2009 - 2026 Copyright © AHTrimble.com ~ All rights reserved

No reproduction or other use of this content

without expressed written permission from AHTrimble.com

No legal, economic, or financial advice is given, no expertise to be assumed.

I may receive compensation from advertised/mentioned products on this website.

See Content Use Policy for more information.

Disclaimer:

The thoughts and opinions expressed in these articles are based on personal observations, experiences,

and independent research. They are intended for informational and thought-provoking purposes only.

I am not an economist, financial advisor, attorney, accountant, or licensed professional.

Nothing contained herein should be considered financial, legal, investment, or tax advice.

Every family’s situation is different, and readers should do their own research and

seek qualified professional guidance before making important decisions.

These writings simply reflect one person’s attempt to better understand the challenges facing

ordinary families and explore practical ideas related to resilience, preparedness,

personal responsibility, and regaining control over everyday life.